Evolution can't get a break!

Value trap or opportunity

Evolution AB came out with its quarterly results, and the stock is down c. -9%. They can’t seem to get a break. There was enough there for both bears and bulls. Don’t expect to outperform the market when everyone agrees or when everything looks rosy. The market prices that all in. It’s when there isn’t a consensus and disagreement that provides an opportunity. I think that’s the case here, and I increased my position in the stock.

Main points from today’s release:

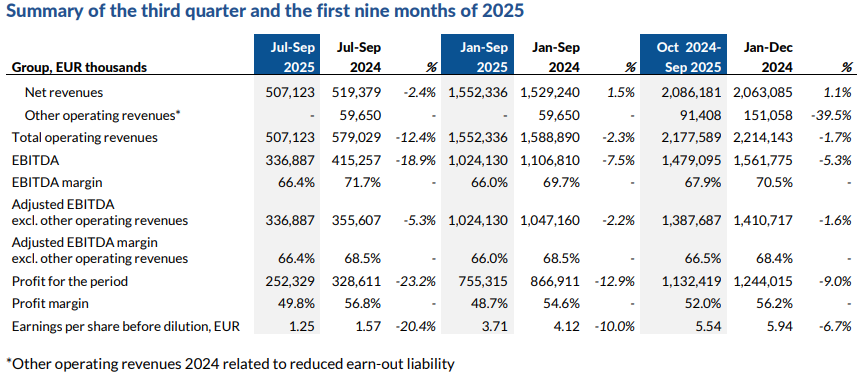

Revenues dropped -2.4% but in constant currency revenues actually grew +3.9%. Another positive is that the RNG revenues are up 4.1%.

EBITDA margin is lower compared to last year (66.4% vs 68.5% in 3Q24), but sequentially, there is an improvement. 1Q25: 65.6%, 2Q25: 65.9%, 3Q25: 66.4%. Cost control kicked in with lower personnel expenses due to lower headcount. On the negative side, “gross profit” per employee is down -0.1% sequentially (This isn’t a company number but a number I calculate as Revenue minus Personnel Expenses).

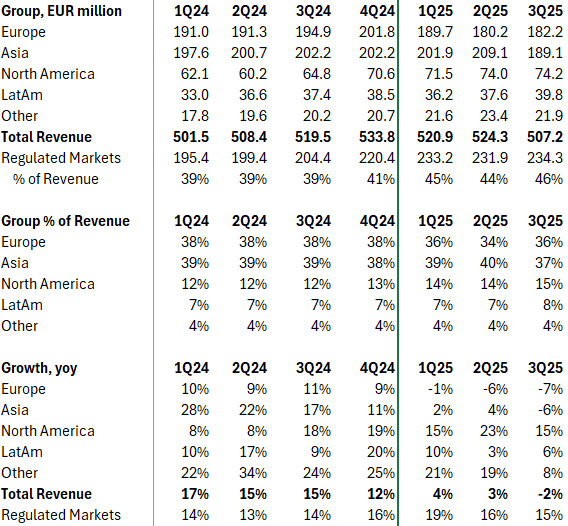

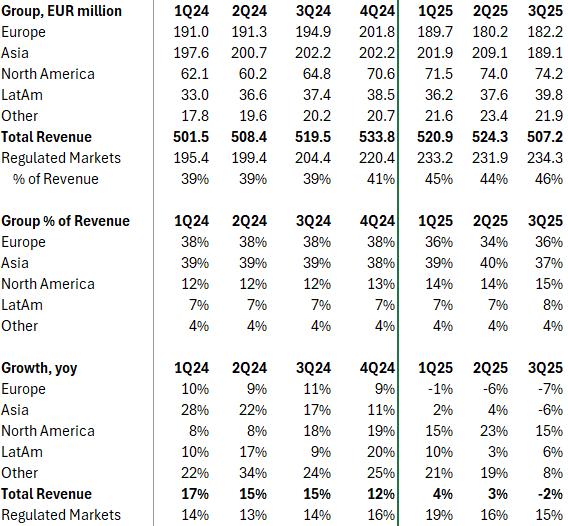

Europe revenues are down -7% yoy but are actually up 1% sequentially. I see this as a positive because we have a base for Europe that saw its revenues drop from the ring-fencing measures the company implemented. This is creates a stronger company in my opinion and hence a positive.

Asia was a big negative. After Q2 where the company returned to growth, we see a decline in revenues from the region. So it looks like the cybercrimes and hijacking of video streams are still an issue. In their effort to fight this, they may have been a little to strict in their measures, which resulted in a negative effect. The company had this to say: “We continue to fight the cyber criminality that has affected our business there for too long, and during the quarter we didn’t progress as much as we would have wanted. The fight is a constant balancing act between taking countermeasures that are too stringent – which create issues for legitimate end-users – and too light, which don’t yield the desired effects. During the third quarter, we overextended our countermeasures and our revenue was affected negatively.”

North America continues to deliver double-digit growth yoy.

Initially announced 2 days ago, the company mentioned today as well that Playtech (a competitor) was behind the ‘short-seller’ report from four years ago. The company is taking legal action against Playtech, whose shares dropped -30% on the news (see here)!

Reiterated guidance of 66-68% EBITDA margin but Asia remains volatile. Capex forecast for 2025 is EUR 140m

Dividend policy is to pay a minimum of 50% of net profit with 100% of excess cash distributed.

Intent to do EUR 500m of share repurchases in 2025

I’m not afraid of the competition. The company is coming out with 110+ new games in 2025. They are the market leader with the best development team, led by Todd Haushalter - the Steve Jobs of Gaming.

Last twelve months FCF was EUR 1,142 or c.9% of Enterprise Value. That’s way too cheap for the quality and position of this company. Assuming EUR 1,000, a 3% growth, and 9% WACC gives you roughly an intrinsic value of SEK 960 compared to roughly SEK 660 today. Either this is an opportunity or I’ve got this very wrong!

Risks include:

Asia (as mentioned)

A longer adjustment period for revenues, as further regulation could result in a repeat of Europe (but elsewhere). Ring fencing, stricter measures for players, or simply stop supplying certain clients because of regulation could hit revenues temporarily as the country/region adjusts to the new status. Over time this problem will turn into a benefit as investors don’t have to worry about this.

Lower margin due to higher opex as a result of regulation. For example, if a studio is required to be local then that would be more expensive versus streaming in size from a cheaper location.

If you are a shareholder, I’d love to hear what you did today. Let me know in the comments!

Find your next idea, chat with experts, and join our community of investors.

Check it out: https://fatalphavalue.com/online

Disclaimer: Not investment advice. Do your own work! This substack is not operated by a broker, a dealer, a registered investment adviser, or a regulated entity. Under no circumstances does any information posted represent a recommendation to buy or sell a security. In no event shall the author be liable to anyone reading this post for any damages of any kind arising out of the use of any content available in this post. Past performance is a poor indicator of future performance. All the information on this substack and any related materials is not intended to be, nor does it constitute investment advice or a recommendation. All materials and information you obtain here are exclusively for informational purposes and do not constitute an offer or solicitation to provide any investment services to investors based in the U.S. or elsewhere.