Is crime snatcher Palantir worth it?

Valuation of Palantir

According to Wikipedia, a palantir is one of several indestructible crystal balls from The Lord of the Rings. The word means ‘far’ and ‘watch over’. For my friend GL, who asked me to take a look, it means $$$. I can’t help but cringe at the 195x P/E ratio, but I promised to be fair.

In simple terms, Palantir acts like a super detective that takes clues from everywhere, instantly connects them, and shows investigators the full picture. Palantir technology was used to help identify the Boston Marathon bomber suspects, by financial investigators to track Bernie Madoff’s Ponzi scheme, and to help find Osama Bin Laden! Sounds like big brother tech, and there are probably some ethical issues here. GDPR? In any case, I plan to provide some perspective on the current market value of the stock and what needs to happen to make this look attractive.

Market Info

Ticker: PLTR

Stock Price (Local): 107.78

52-W High (February 19, 2025): 125.41

52-W Low (May 10, 2024): 20.50

5 Year Beta: 2.74

Avg Volume (3-month, millions): 110.4

Avg Volume (USD, millions): $11,901.6

Shares outstanding (basic): 2,345

Enterprise Value

Market Cap (USD, millions): $252,783

Plus: Total Debt $239 of which Leases $239

Plus: Minority Interest $91

Less: Cash and ST Investments -$5,230

EV (USD, millions): $247,883

Key Valuation Metrics

P/E forward 195x

EV/EBITDA forward 153.4x

Dividend Yield 0.0%

Key Persons

Co-Founder & Chairman: Thiel, Peter

Co-Founder, CEO & Director: Karp, Alexander

Co-Founder, President, Secretary & Director: Cohen, Stephen

Board of Directors, Chairman: Thiel, Peter

Top Holders

Vanguard: 9%

BlackRock: 7%

Peter Thiel: 4%

State Street: 4%

Alexander Karp: 2%

Geode Cap Mgmt: 2%

Renaissance Tech: 1%

Stephen Cohen: 1%

Stock Performance

The company listed its shares in September 2020. The stock has outperformed the S&P 500 over all periods and is up c. 43% YTD versus c. -4% for the index.

Aggressive Consensus Assumptions

If we look at consensus estimates for revenue growth for the next three years, we see 31%, 28%, and 33%, respectively. This is a problem for two reasons. Firstly, any misses will affect the stock price, but more importantly, this implies that Palantir is an amazing business. For the stock to be a potential buy, we would have to apply some pretty aggressive rates. So what do we do?

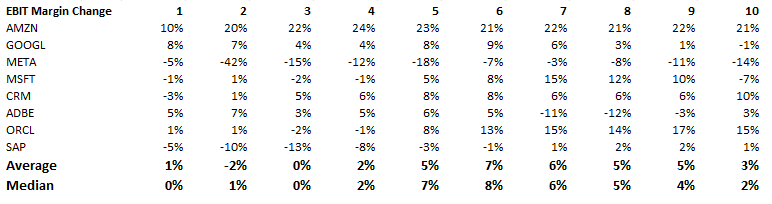

One way to think about this is to consider how much did successful c. $3 billion in revenue companies grow in the subsequent years. Below is a list of well-known tech companies, along with their 10-year CAGR following a year where revenues were closest to the $2.8b mark.

Meta: 46%

Google: 35%

Amazon: 29%

Microsoft: 26%

Salesforce: 26%

Oracle: 15%

SAP: 13%

Adobe: 9%

I have trouble seeing Palantir matching Microsoft. So let’s assume a 20% CAGR to start with.

Another thing I’d like to point out regards the revenue per customer. The company gives the average revenue from the top 20 clients, and this has grown at double digits (+18% in FY24). Total customers have also grown from 139 in FY20 to 711 in FY24. But if we measure the average revenue per client, then we will notice this is in decline. Of course, this isn’t worrisome as new clients haven’t yet adopted many features and hence the average revenue is low, but still it’s probably worth keeping in mind. Anyone doing a deep dive should attempt to model out the clients into new and mature.

Consensus assumes an expansion of the operating margin. Consensus also adds back Stock-Based Compensation (SBC) to their estimates. In my opinion SBC is an expense, and so I reduce the consensus operating profit by an estimation of SBC based on the FY24 % of revenues. This adjusted consensus operating margin rises from 10.8% to 19.2%. Is this 8.4% expansion reasonable?

Again, I look at the companies mentioned above. In the table below, we see how much their margin expanded. This peaked in year 6, where the average was 6.8% and the median was 7.8%. For our exercise, I’ll accept the 8.4%.

Forecasts and DCF Valuation

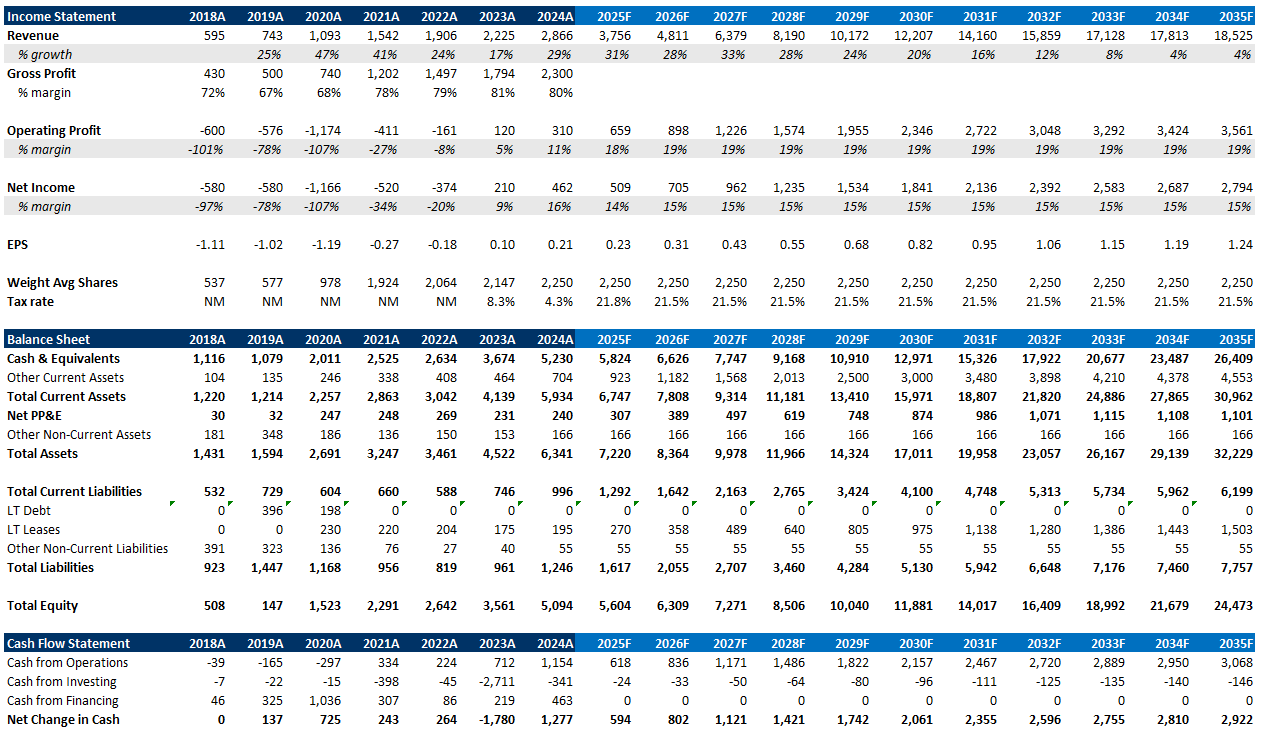

I use the consensus revenue growth mentioned in the previous section for the first 3 years and then fade it so that the 10-year CAGR ends up at 20%. For the terminal value I use 4%. Adjusted operating profit is kept constant at 19.2% after the first 3 years. The other assumptions made were in line with the consensus or historical.

The model results in an intrinsic value of $132, which implies that the stock is trading at a discount to its intrinsic value.

The problem that I have with this valuation is that there is no margin of safety. Everything has to work out perfectly. What happens if the forward 10-year CAGR is 15%? All else equal, the intrinsic value drops to $103, which is roughly on par with the current market value. So, to be interested in PLTR today, you need to believe that at a minimum, revenues will grow at a 15% CAGR for the next decade, and the EBIT margin will expand by 8.4%.

What if the 15% CAGR happens but after an initial expansion of margin, it declines by 2% so that the long-run adjusted EBIT margin is 17.2% (instead of 19.2%). Then the intrinsic value drops to $97.

According to a McKinsey study of 5,000 companies (over 2009-19) only 1 in 8 grew by a rate higher than 10%. So what if the 10-year CAGR is a little lower at 12%? That would still place Palantir in the ‘Hall of Fame’ but the intrinsic value would be 83.

Personally, I don’t find the current market value compelling enough to investigate further. Someone would have to very thoroughly understand the business, be confident that the TAM is large enough, and that the company can retain whatever tech advantage it currently holds. Out of the original creators of Palantir’s prototype, only Stehn Cohen (Stanford, Computer Science) remains. Nathan Gettings (Paypal engineer at the time) and Joe Lonsdale (Stanford, Computer Science) left.

So for me, it’s a pass at the moment. Convince me I’m wrong in the comments!

If you like this article, please subscribe so more people can find it!

Disclaimer: Not investment advice. Do your own work! This account is not operated by a broker, a dealer, a registered investment adviser, or a regulated entity. Under no circumstances does any information posted represent a recommendation to buy or sell a security. In no event shall the author be liable to anyone reading this post for any damages of any kind arising out of the use of any content available in this post. Past performance is a poor indicator of future performance. All the information on this substack and any related materials is not intended to be, nor does it constitute investment advice or a recommendation. All materials and information you obtain here are exclusively for informational purposes and do not constitute an offer or solicitation to provide any investment services to investors based in the U.S. or elsewhere.

Well reasoned overview with nice detail!

You have pointed out that the owner of these shares at the current price is not holding an investment, but rather a trade that depends on perfection and sentiment. Well done!

I lucked into the Series B for this company through an investment in Thiel’s former hedge fund, Clarium. Unfortunately I sold it before the IPO. I recall that the Pentagon disputed their claim to have “found” Bin Laden, which made me question a lot of their other claims. Also this is another stock like Tesla that rocketed when Trump won, as if their principals’ support for his campaign would lead to lots of Federal deals. In this case unlike Tesla the puffery hasn’t been knocked out of the price yet.