Japanese Stock Ideas

A look at JVC Kenwood & Nippon Paint

I’m looking at JVC Kenwood and Nippon Paint. Both are listed in Japan, which will be the topic of my next podcast. I’ll be interviewing Robert Karas, who recently went to Japan, and will share his thoughts on the country and those two companies. Robert is the Chief Investment Strategist of Bank Gutmann.

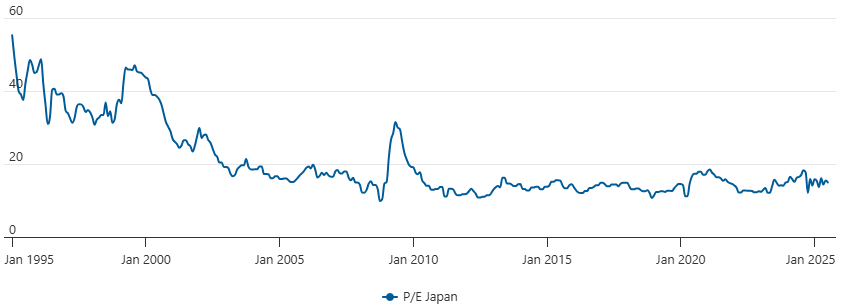

While the Nikkei 225 has been ripping higher for at least a decade, if we look at the long-term, we see that it took c. 35 years to make a new all-time high!

As you see from the chart below from worldperatio.com, the multiple has come down significantly. The index had peaked at a P/E of 60+, depending on what earnings data you used. Clearly unsustainable.

While the index made a new all-time high, it has been moving sideways over the last year.

Let’s start by taking a look at Nippon Paint:

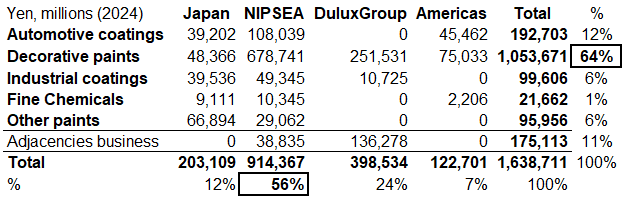

One of the largest paint makers in the world, with the majority of sales coming from decorative paints (64%). These are commonly used to make surfaces look nice (eg. walls, windows, doors) while offering basic protection. The next 2 most important categories are Automotive (12%), and Adjacent products such as adhesives and sealants (11%).

NIPSEA (aka Nippon Paint South East Asia - basically Asia ex-Japan) is the largest geography at 56%. NIPSEA is the most profitable segment at 14% operating margin. DuluxGroup (that covers Australia, New Zealand, and parts of Asia) is the second largest at 24%. It was purchased from AkzoNobel in 2019 for around ¥300 billion (c. ¥330 including debt). DuluxGroup now generates c. ¥40 billion in operating profit (10% margin). Japan also has a 10% margin, while the Americas are the least profitable at 6%. Keep in mind that in March 2025, Nippon completed an additional acquisition that is expected to add to sales and EPS. AOC (involved in Coatings, Adhesives, Sealants, and Elastomers) was acquired at EV/EBITDA 8.2x (or ¥630 billion)

Market Info

Company Name: Nippon Paint Holdings

Ticker: TSE:4612

Stock Price (Local): ¥1,227.00

52-W High (October-29-2024): ¥1,258.50

52-W Low (August-05-2024): ¥807.80

5-Year Beta 1.16

Avg Volume (3-month, millions): 2.5

Avg Volume (USD, millions): 21.2

Shares outstanding (basic, millions) 2,349

Enterprise Value

(Figures on the left are in USD, and on the right are in JPY)

Market Cap (millions): $19,558 | ¥2,882,038

Plus: Total Debt $9,514 | ¥1,424,646 of which Leases $647 | ¥101,782

Plus: Minority Interest $130 | ¥19,458

Less: Cash and ST Investments -$2,035 | -¥304,702

EV (millions): $27,167 | ¥4,021,440

Key Valuation Metrics

P/E forward 17x

EV/EBITDA forward 12.4x

Dividend Yield 1.3%

Key Persons

As you’ll notice, there are 2 heads:

Representative Executive Officer, Co-President & Director: Wakatsuki, Yuichiro Representative Executive Officer, Co-President & Director: Wee, Siew Kim

Corporate Officer, Deputy CFO, and GM of Finance & Accounting: Kudo, Shuichi Board of Directors, Chairman: Goh, Hup Jin

Top 5 Institutional Holders

EdgePoint Investment Group 2%

Nissay Asset Mgmt Corp 2%

BlackRock 2%

Vanguard Group 2%

Norges Bank Inv Mgmt 2%

Wuthelam Holdings (Goh family) is now the controlling shareholder of Nippon Paint with a 59% stake. Mr. Goh is the chairman.

Stock Performance

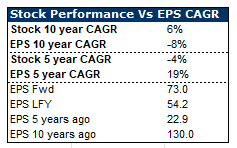

The stock hasn’t been performing that well; however, earnings have been compounding at 19% over the last 5 years.

For those who bought a year ago, they are sitting on a nice double-digit profit:

But investors from 5 years ago are still at a significant loss:

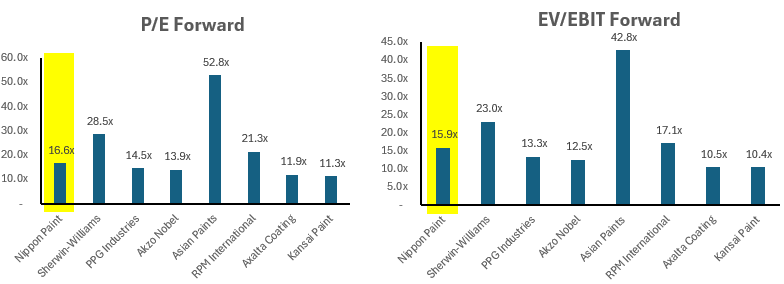

If we exclude Asian Paints, the stock trades at the average multiple of the group.

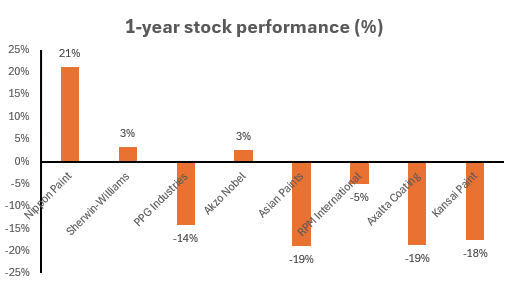

The stock has been the best performer over the last year:

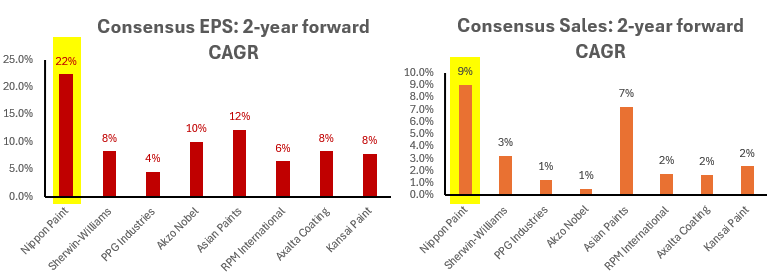

Possibly due to consensus expectations for forward growth in both top and bottom line:

Looking at the 2025 consensus numbers and some historical figures for working capital and capex, I put my back-of-the-envelope FCF at ¥160 billion. Incorporating the low rates in Japan and a 3% perpetuity gives me a value c. ¥1,300 (above the current market price). 2026 consensus for FCF is c. ¥180 billion, which would take us to c. ¥1,500. The single-digit ROE and ROIC, as well as the family majority ownership, certainly don’t excite me, so I’m looking forward to seeing how Robert views this.

Now let’s take a look at JVC Kenwood.

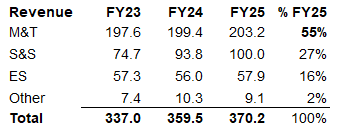

The Japanese electronics company was the result of a merger between JVC (Victor Company of Japan) and Kenwood. It operates through three main segments: Mobility & Telematics Services (M&T), Safety & Security (S&S), and Entertainment Solutions (ES). In the M&T segment, the company produces automotive electronics such as car audio systems, car navigation, dashcam recorders, and other in-vehicle devices. The S&S segment provides professional communications and security equipment, such as two-way radio systems for public safety (police, fire, etc.), professional video surveillance systems, commercial audio equipment, and medical display monitors. The ES segment includes consumer and professional A/V products and media. From projectors, video cameras, headphones, and home audio, to content services like music/video software distribution and CD/DVD production.

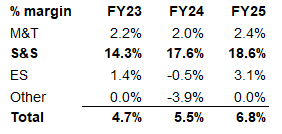

M&T is the largest segment, generating 55% of revenues.

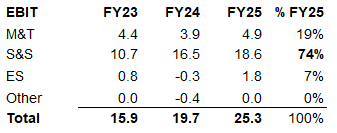

However, S&S generates 74% of the company’s operating profits.

This is because S&S has margins in the high teens, while the other segments are in the lower single digits. Activist alert?

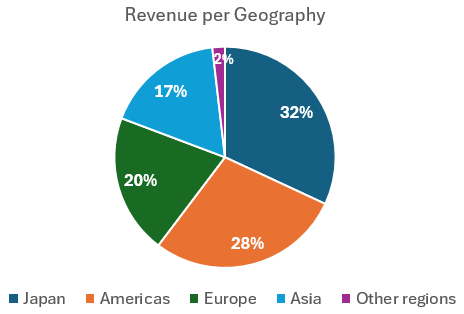

An international company with revenue from all around the world:

Market Info

Company Name: JVC Kenwood

Ticker: TSE:6632

Stock Price (Local): ¥1,131.00

52-W High (January-30-2025): ¥1,832.00

52-W Low (August-01-2024): ¥854.00

5-Year Beta: 0.78

Avg Volume (3-month, millions): 1.1

Avg Volume (USD, millions): 8.5

Shares outstanding (basic, millions): 146

Enterprise Value

(Figures on the left are in USD, and on the right are in JPY)

Market Cap (millions): $1,123 | ¥165,536

Plus: Total Debt $336 | ¥50,374 of which Leases $96 | ¥14,405

Plus: Minority Interest: $42 | ¥6,295

Less: Cash and ST Investments -$325 | -¥48,597

EV (millions): $1,177 | ¥173,608

Key Valuation Metrics

P/E forward 11x

EV/EBITDA forward 4.5x

Dividend Yield 1.6%

Key Persons

President, CEO & Representative Director: Eguchi, Shoichiro

CFO, Senior Managing Exec Officer & Representative Director: Miyamoto, Masatoshi Managing Executive Officer, CTO, CISO & Director: Sonoda, Yoshio

Board of Directors, Chairman: Hamasaki, Yuji

Top 5 Institutional Holders

Asset Management One: 7%

Sumitomo Mitsui DS Asset Mgmt: 4%

Nomura Asset Management: 4%

Vanguard Group: 4%

American Century Inv Mgmt: 3%

Stock Performance

The stock has done well, rising in line with EPS.

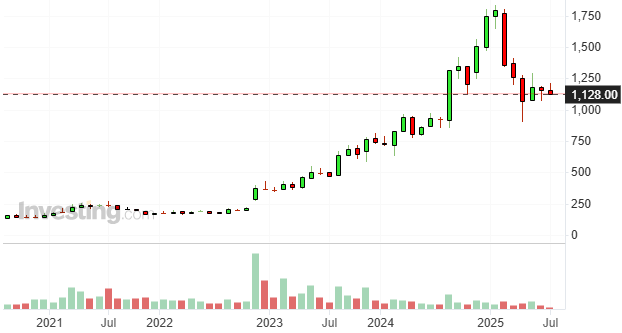

Nice gains over the last 5 years:

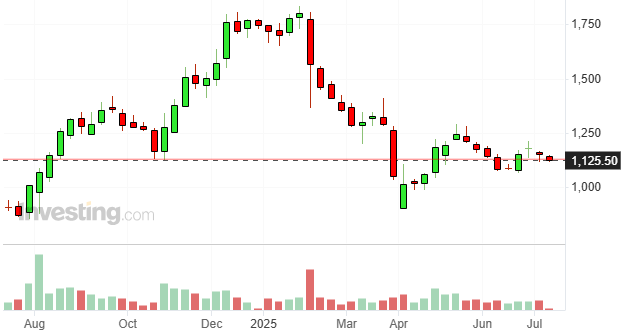

But has come off of its highs, trading significantly lower:

JVC Kenwood is probably the more interesting story because S&S looks like a niche segment where it could possibly do well. If they can maintain the FCF of ¥10 billion and build on it, the stock is possibly worth around c.¥1,400 using management WACC of 7% (see here). If this were in Europe, there would be an activist case for selling or spinning off Entertainment, IPOing S&S as a pure play, and returning capital to shareholders. But perhaps there are cross-holdings and cultural issues... Perhaps Robert can shed some light here.

So if you want to hear more about Japan and these two stocks, make sure you subscribe or come back in a few days when I’ve posted the podcast with Robert Karas!

Disclaimer: Not investment advice. Do your own work! This account is not operated by a broker, a dealer, a registered investment adviser, or a regulated entity. Under no circumstances does any information posted represent a recommendation to buy or sell a security. In no event shall the author be liable to anyone reading this post for any damages of any kind arising out of the use of any content available in this post. Past performance is a poor indicator of future performance. All the information on this substack and any related materials is not intended to be, nor does it constitute investment advice or a recommendation. All materials and information you obtain here are exclusively for informational purposes and do not constitute an offer or solicitation to provide any investment services to investors based in the U.S. or elsewhere.