UBS is wrong on Palantir

More pain to come

UBS released a report on June 15, setting a $200 price target based on 77x 2027E FCF. That implies a growth expectation similar to Cisco in 1999. CSCO shareholders had to wait 26 years to get to breakeven! Investors who are long PLTR must believe the company will be one of the greatest ever. I warned my readers in April (see here) when Palatir, and I’m warning them again. The numbers don’t make sense to me…

Firstly, I think UBS’s actual number is $191, and they just rounded it off to $200. No harm there, as this isn’t an exact science. Using their published equity FCF yield (2.0%), we can back that out. I use 2.04% to give the maximum FCF implied of $6.7B. Consensus is at $6.4B.

EV based on 72x FCF 2027E implied = $483b

+ Net Cash of $8b

= Equity value = $491b

Current # of shares outstanding = 2,571

Share value = $191

Typically, analysts don’t include Stock-Based Compensation (SBC), so their numbers have a boost we need to adjust for. In the last 3 years, the weighted average number of shares grew by 4.1%, 4.8%, and 5.3%. Assuming 5% for the next 2 years implies that the # of shares outstanding will grow to 2,835.

Adjusted # of shares outstanding = 2,835

Share value = $173

So if you assume the shares will trade at 72x FCF ‘27 in 2 years, buying at c.$120 will yield an IRR of 20%.

“But Sophocles… the market adjusts quickly! We won’t need to wait 2 years but 1.”

Ok, well then in that case, the share value is $182, and the IRR is 50%.

One of the best companies?

UBS sees revenues rising to $30b in 2030E. That means revenues must compound at a 46% CAGR, and Palantir must be one of the greatest companies ever. Below are the revenues of Meta, Alphabet, Microsoft, and Amazon when they were at a similar size to Palantir. A 46% CAGR would be better than Microsoft and Amazon.

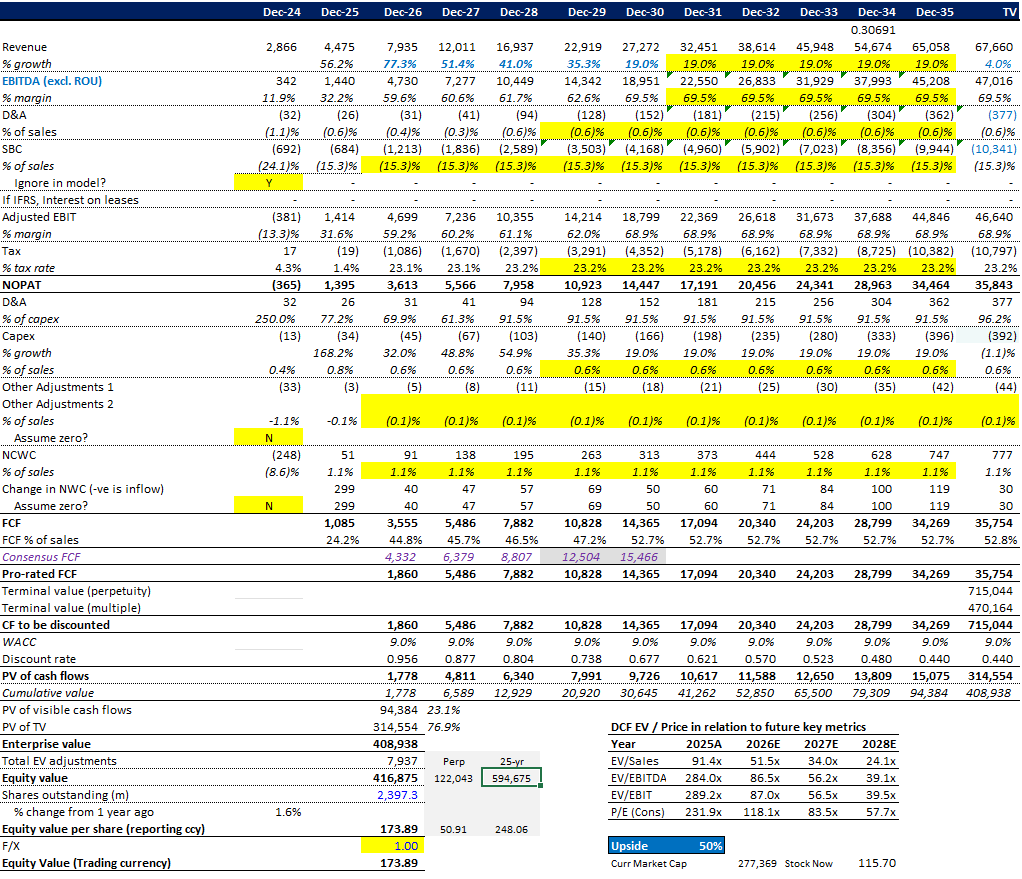

Incorporating UBS assumptions

I don’t have the UBS model or the full assumptions, but I have seen their sales revenue and EBIT estimates, and I will use those. For the rest, I’ll take consensus numbers. Revenues are expected to grow by 19% in 2030, and I’ll assume they continue at 19% through 2035. After that, I’ll calculate a terminal value based on 4% top-line growth. This means that for the 10-year period, PLTR will compound at an assumed 31% CAGR. For perspective, see below the equivalent 10-year growth of Meta, Alphabet, Microsoft, and Amazon at similar sizes. Again, we have to assume that PLTR is one of the greatest companies ever!

So, if we ignore SBC and assume revenue grows at a 31% CAGR and EBITDA margin expands from 32% in 2025 to 70% in 2030+, we get an intrinsic value of $174... (fyi, I’m using a 9% WACC).

You know what this reminds me of? Analysts’ assumptions for Cisco (CSCO) in 1999.

If, instead of listening to Wall Street consensus, you’d rather hear 12 professional investors present 12 high-conviction ideas that are often uncorrelated with the typical sell-side view, join the 3rd FatAlpha Value Online Conference on October 22–23. The €99 Early Bird expires in the next 24 hours. 👉 https://fatalphavalue.com/online

Cisco Thoughts

Cisco reached a peak valuation of c.$380B (see here). I took the 1999 numbers for revenue, EBIT, depreciation, and capex and extrapolated forward for the next 10 years, changing only the top-line growth. To reach the $380B figure, I’d have to grow revenue at a 34% CAGR for 10 years! In reality, Cisco only grew at a 7% CAGR! Not only that! EBIT margin was 4% lower… So the probability UBS is right is low in my opinion.

What is the market telling us?

Spoiler alert. It’s still aggressive.

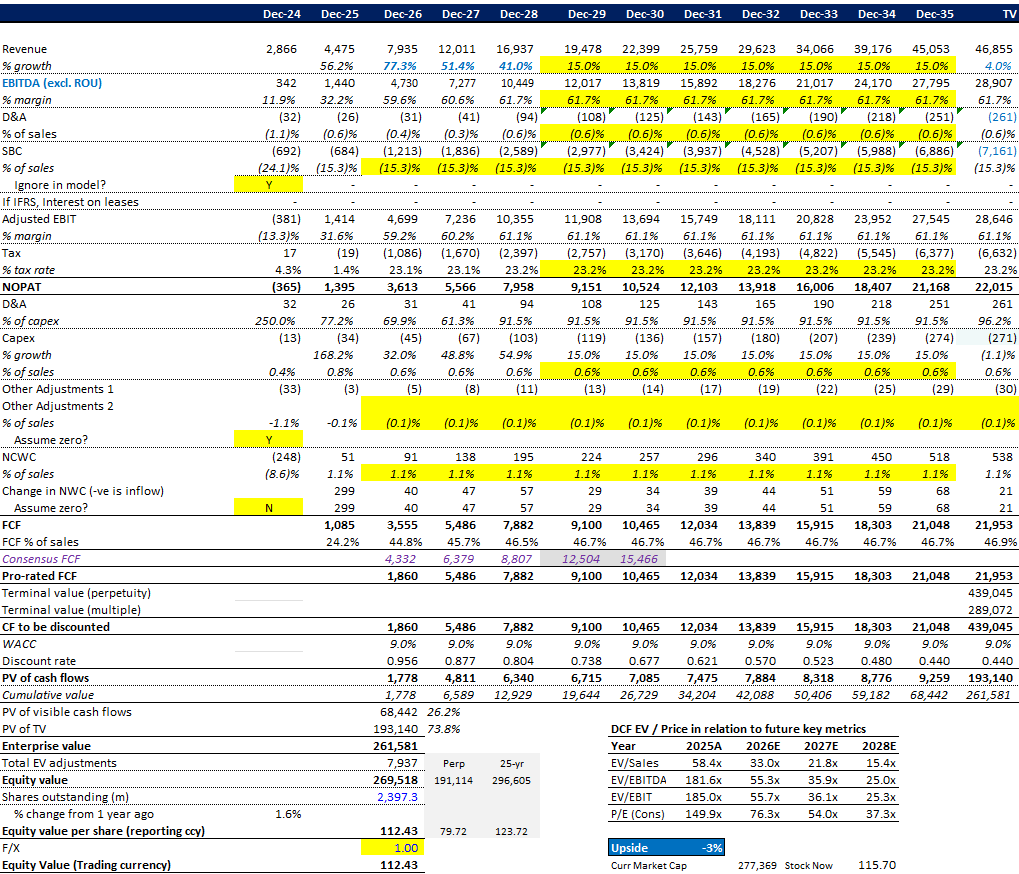

If we use UBS’ figures through 2028, then grow the top line by 15%, and ignore SBC and any dilution, we get an intrinsic value of c. $112. This means we believe in a 10-year CAGR of 26% …

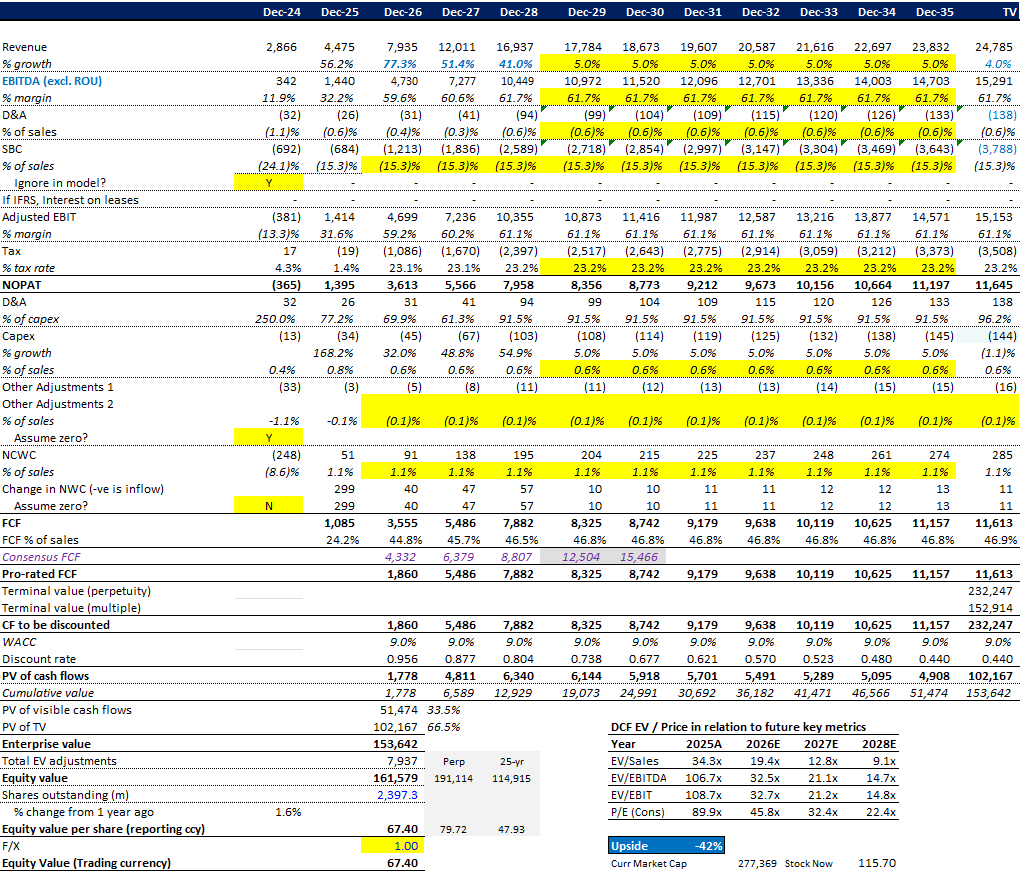

That’s not something I can stomach. Investing is about probabilities. Double-digit revenue growth is not common. Only 1 in 8 companies grows revenue at a 10-year CAGR higher than 10%. But let’s say Palatir is exceptional and it achieves an 18% CAGR (instead of 26%), then intrinsic value still drops to under $70. So I think it’s more likely the stock will weaken further from here.

To put this in blackjack terms, you could split tens and hit 2 aces and win, but I don’t want to take that gamble. The math just doesn’t support it.

Sophocles

P.S. Bonus for early bird signups: 6 replay recordings from previous events. Check it out: https://fatalphavalue.com/online

Disclaimer: Not investment advice. Do your own work! This account is not operated by a broker, a dealer, a registered investment adviser, or a regulated entity. Under no circumstances does any information posted represent a recommendation to buy or sell a security. In no event shall the author be liable to anyone reading this post for any damages of any kind arising out of the use of any content available in this post. Past performance is a poor indicator of future performance. All the information on this substack and any related materials is not intended to be, nor does it constitute investment advice or a recommendation. All materials and information you obtain here are exclusively for informational purposes and do not constitute an offer or solicitation to provide any investment services to investors based in the U.S. or elsewhere.