Undervalued Gold Miner?

Valuation of G Mining

Goldbugs are partying as the shiny metal is ripping higher. But this isn’t the first time. From 2004 to 2011, gold went from c. 400 to c. 1900. So, imagine it’s 2011 and you bought gold at around $1,900. Unless you averaged down, you had to wait until this year to make some money! Not really a spectacular return if you consider the holding period.

Regardless, perhaps this time is different (famous last words), and gold is on a new run. If it went c. 5x higher as it did in the 2004-11 period mentioned, then gold could end up at c. 10k. Sounds crazy, but if you are around markets long enough, then nothing will surprise you. Those of you who have read my pieces know that I avoid crazy assumptions, so how about we just assume gold remains at this level for the next decade? And let’s look at a potentially undervalued gold mining company, both compared to peers and to discounted cash flow.

Side note: If you like great stock ideas (who doesn’t, right?) then check out the Online event I’m organising at the end of the month (click here) with an amazing roster of fund managers and experts. I’ve been organising exclusive in-person events for the past decade. My flagship September event has been fully booked since February. Through this Online event, I’m making high-quality content previously reserved for a select group of investors available to everyone. Check it out: https://fatalphavalue.com/online

Market Info

Company Name: G Mining Ventures Corp.

Ticker: TSX:GMIN

Stock Price (Local) 18.45

52-W High (June-04-2025): 22.30

52-W Low (September-06-2024): 7.89

5 Year Beta: -0.59

Avg Volume (3-month, millions): 1.0

Avg Volume (USD, millions): 14.2

Shares outstanding (basic, millions): 226

Country of Incorporation: Canada

Trading Currency: CAD

Filing Currency: USD

Enterprise Value

(Figures on the left are in USD, and on the right are in CAD)

Market Cap (millions): $3,070 | CAD 4,174

Plus: Total Debt $113 | CAD 113 of which Leases $1 | CAD 1

Less: Cash and ST Investments -$149 | -CAD 149

EV (millions): $3,034 | CAD 4,138

Valuation Metrics

(These aren’t appropriate for mining unless it is a very large miner with a significant portfolio of assets, but I show here for consistency with my prior posts).

P/E forward: 13x

EV/EBITDA forward: 8.2x

Dividend Yield: 0.0%

Key Persons

Founder, CEO, President & Director: Gignac, Louis-Pierre

Founder & Senior VP of Corporate Strategy: Petkovic, Dusan

VP of Finance & CFO: Lafleur, Julie

Board of Directors, Chairman: Gignac, Louis

Executive management appears to have a long history within the mining industry and has a good history of building projects on time and within budget.

Top Holders

La Mancha Holding: 16%

Van Eck Associates: 8%

Franco-Nevada 7%

Gignac family 6%

Franklin Resources: 3%

First Eagle Inv Mgmt: 3%

ASA Gold and Precious Metals: 3%

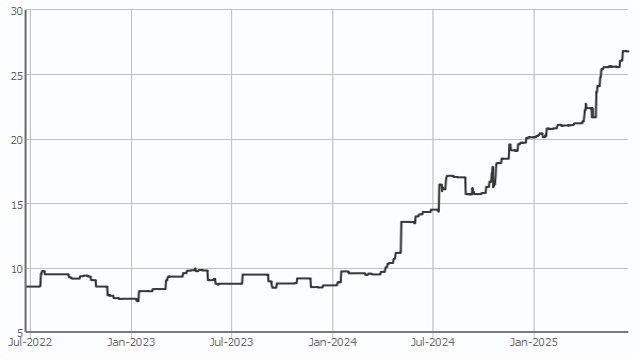

Stock Performance

Year to date, the stock is up c. 70% while gold is up c. 29% and the S&P 500 c. 2%

This will be a two-part series. In this short note, I will share some thoughts on G Mining (GMIN) which is listed in Toronto. Keep in mind that this is an intro and not a deep dive. My goal here is to learn the basics of the company, and investigate the potential opportunity. In the second part, which I expect to publish this weekend or Monday, I’ll share a video interview that I will conduct on Saturday with Samir Mohamed. That interview will be for my podcast “No Fluff, Just Ideas” and will be available on this Substack, as well as YouTube, Spotify, and Apple Podcasts. Samir has presented at MOI Global’s online conferences for many years, as well as the conferences I organise in Cyprus and Asia. He has been managing his own capital for over a decade, so he puts his money where his mouth is!

G Mining’s business is the acquisition, exploration, development, and operation of mines. In 2024, it started generating revenues from its Tocantinzinho Gold Mine (“TZ Mine”), which is located in Brazil. In 2024, the company acquired 2 projects: 1) Oko West, which was purchased with shares at a transaction valued at CAD 875m at the time, 2) Gurupi with no upfront cost. Neither of these generates any revenue yet.

Oko West (situated in Guyana) is expected to produce 350,000 ounces of gold a year for 12.3 years. This is expected to significantly boost production by almost 200% and is an important driver of this story.

When Brazilian Gurupi goes online, they will pay BHP Grouphe seller) a 1.0% net smelter return royalty for the first 1 million ounces of gold and then 1.5% thereafter.

Peers

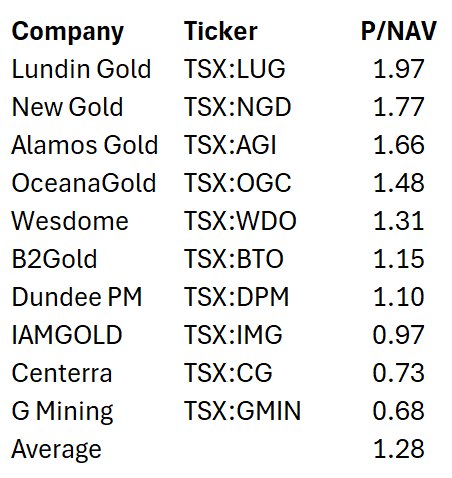

Analyst consensus for GMIN’s NAV per share is CAD 26.79. This has been on the rise as the value increases with the gold price.

If we take the peers from the GMIN investor relations slide above and compare the current stock price to the last consensus NAV, then we see that G Mining has the lowest multiple! It would need to almost double to get to the average!

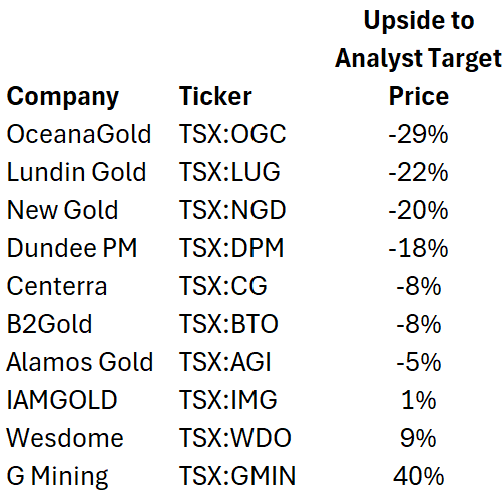

The table below shows the upside each stock has to the analysts’ consensus target prices. As Lundin Gold has a 1.97x P/NAV, we see that analysts have a target price which is -22% lower. G Mining has the highest difference and the stock would need to rise 40% to reach analysts’ target price.

Valuation

But let’s focus on what we do know is generating income: TZ Mine. The company has provided an outlook for 2025 that includes gold production of 175k oz to 200k oz, and AISC of $995 to $1,125 $/oz. Note that Site AISC, which is typically quoted by mining companies, is lower. AISC stands for All-in Sustaining Costs, and it is the cost of running a gold mine at its current rate. Established by the World Gold Council in 2013, it includes mining costs, processing costs, site G&A, royalties and production taxes, as well as sustaining CAPEX (maintenance), reclamation and remediation costs, and corporate G&A directly attributable to sustaining current operations. Not included: CAPEX for new mines or major expansions, depreciation, finance costs, and income taxes.

So we can make some rough assumptions and come out with a valuation. Let’s start by assuming the current gold price of $3,400 remains constant through the period, an AISC of $1,060 (average of outlook), and a 187k oz production (mid outlook). To calculate tax, I deducted depreciation and finance expenses as they are not in AISC. I used a tax rate of 15.25%, which is a special tax status in Brazil that GMIN expect to secure, and a discount rate of 10%. This gives me a $2.1b value.

I then did the same exercise for Oko West, but increased the AISC to $1,123 according to the feasibility study and used a 25% tax (different expected status). I also started the cash flow 3 years from now and included the $972m capex involved to develop. This gives me a $2.4b value. So, the combined value is $4.5b. This doesn’t include any income from Gurupi or from expansion projects on TX that would increase production.

1 USD is roughly CAD 1.37 so the $4.5b translates to CAD 6.2b. Cash offsets debt, but both are relatively small, so they are ignored for this exercise. With 226.2m shares outstanding, the fair value comes out to CAD 27.53 or c. 50% higher than the current market price!

Gold would have to decline to $2,750 as well as NO expanded production from TZ Mine, and ZERO from Gurupi to get the value to the current market price! We will discuss gold, G Mining, and go over the numbers in a lot more detail than I have today. So make sure you come back for part 2 to hear the case from Samir. Post your questions in the comments ASAP, and I’ll ask them on the podcast!

If you want to hear more experts and well-established global fund managers share their ideas then don’t forget to check out the Online Event: https://fatalphavalue.com/online

Disclaimer: Not investment advice. Do your own work! This account is not operated by a broker, a dealer, a registered investment adviser, or a regulated entity. Under no circumstances does any information posted represent a recommendation to buy or sell a security. In no event shall the author be liable to anyone reading this post for any damages of any kind arising out of the use of any content available in this post. Past performance is a poor indicator of future performance. All the information on this substack and any related materials is not intended to be, nor does it constitute investment advice or a recommendation. All materials and information you obtain here are exclusively for informational purposes and do not constitute an offer or solicitation to provide any investment services to investors based in the U.S. or elsewhere.

Dear Sophocles,

Thank you for sharing this compelling investment idea and for building this community—I'm glad I found it. After doing my own due diligence on the company, a few questions came to mind that I was hoping you could shed some light on:

The capital required for the Oko West project is substantial. I'm curious about the potential for shareholder dilution to secure the necessary financing. On a related note, considering Brazil's current fiscal situation, are there any notable tax-related risks that could impact the Tocantinzinho project's cash flow?

Regarding the Oko West project, I'm interested in understanding how the company is mitigating key execution risks in Guyana, specifically around permitting, labor availability, and overall project management. Furthermore, how would you characterize the stability of Guyana's regulatory framework concerning property rights and taxation for a long-term mining project?

I understand that a core part of the investment thesis for GMIN is the Gignac team's stellar reputation for flawless execution. With that in mind, I'm curious how the accounting restatement announced in May 2025, which affected the 2024 earnings, might impact this narrative and investor confidence.

Looking forward to the podcast!