Gems from the Magic Screen

New output from the model

One of my readers commented on a piece (here) I wrote last year, in which I showed the output of a model based on my own twist on Greenblatt’s ‘Magic Formula’. I realized it’s been a while since I ran it, so I decided to a) see what happened to some of these stocks and b) re-run it based on today.

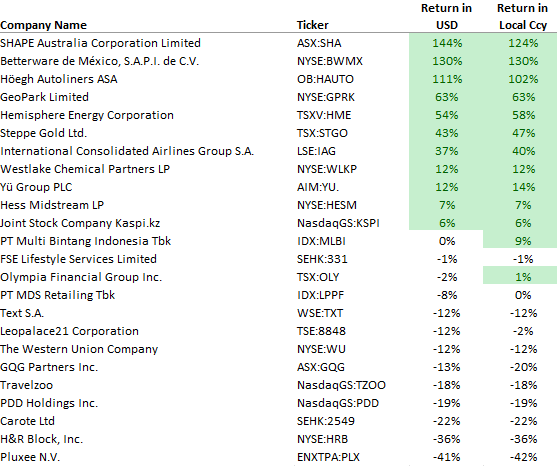

Big Winners!

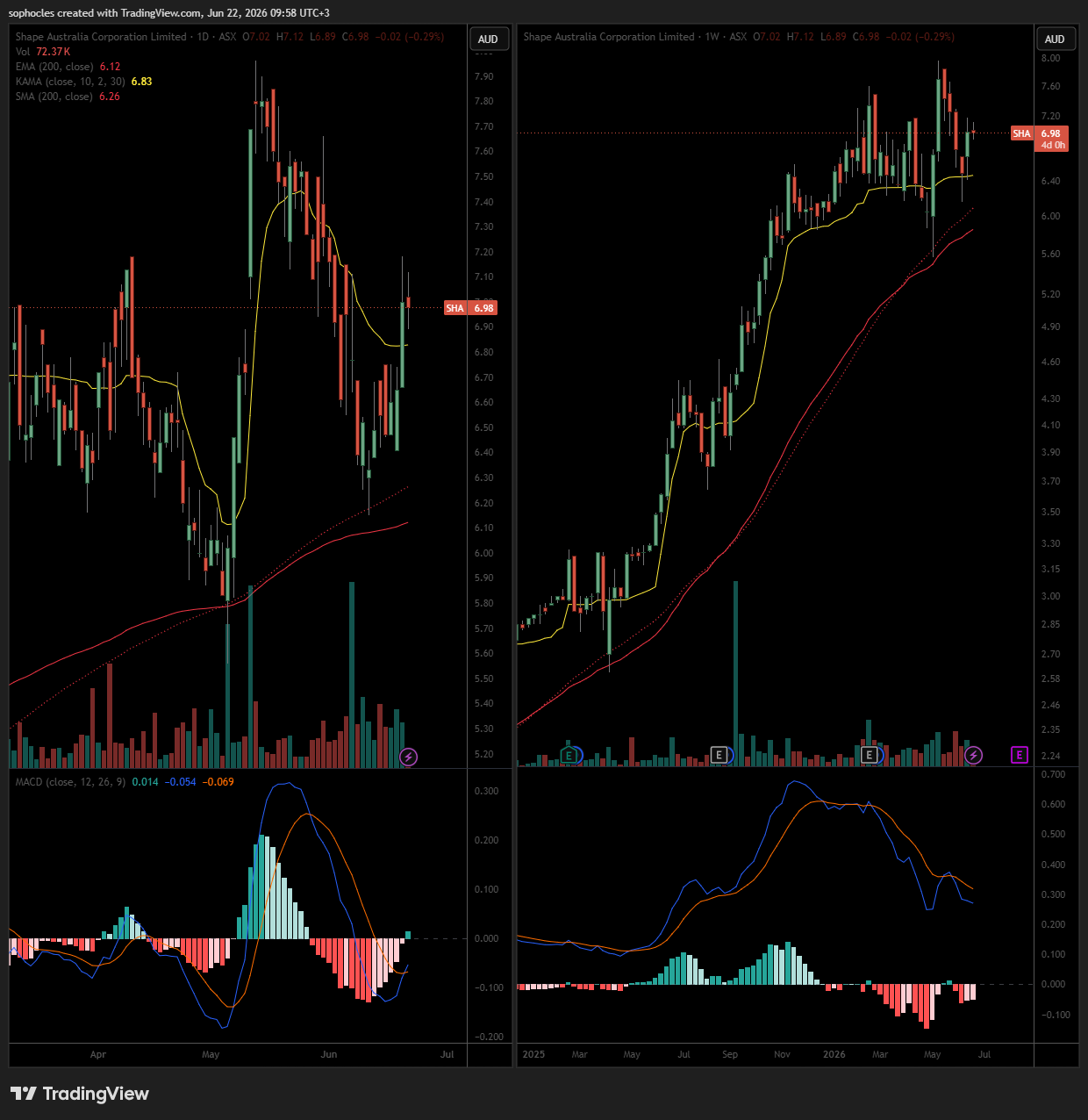

The model kicked out some very big winners! I published the article on May 29 2025, so I measured the performance from that date until today. That’s almost 13 months. Shape Australia rose 144% in USD and 124% in local terms, as both revenue and earnings rose in the double digits for the construction services provider. The chart below shows the weekly performance over the last year (on the right) and more recent daily activity on the left.

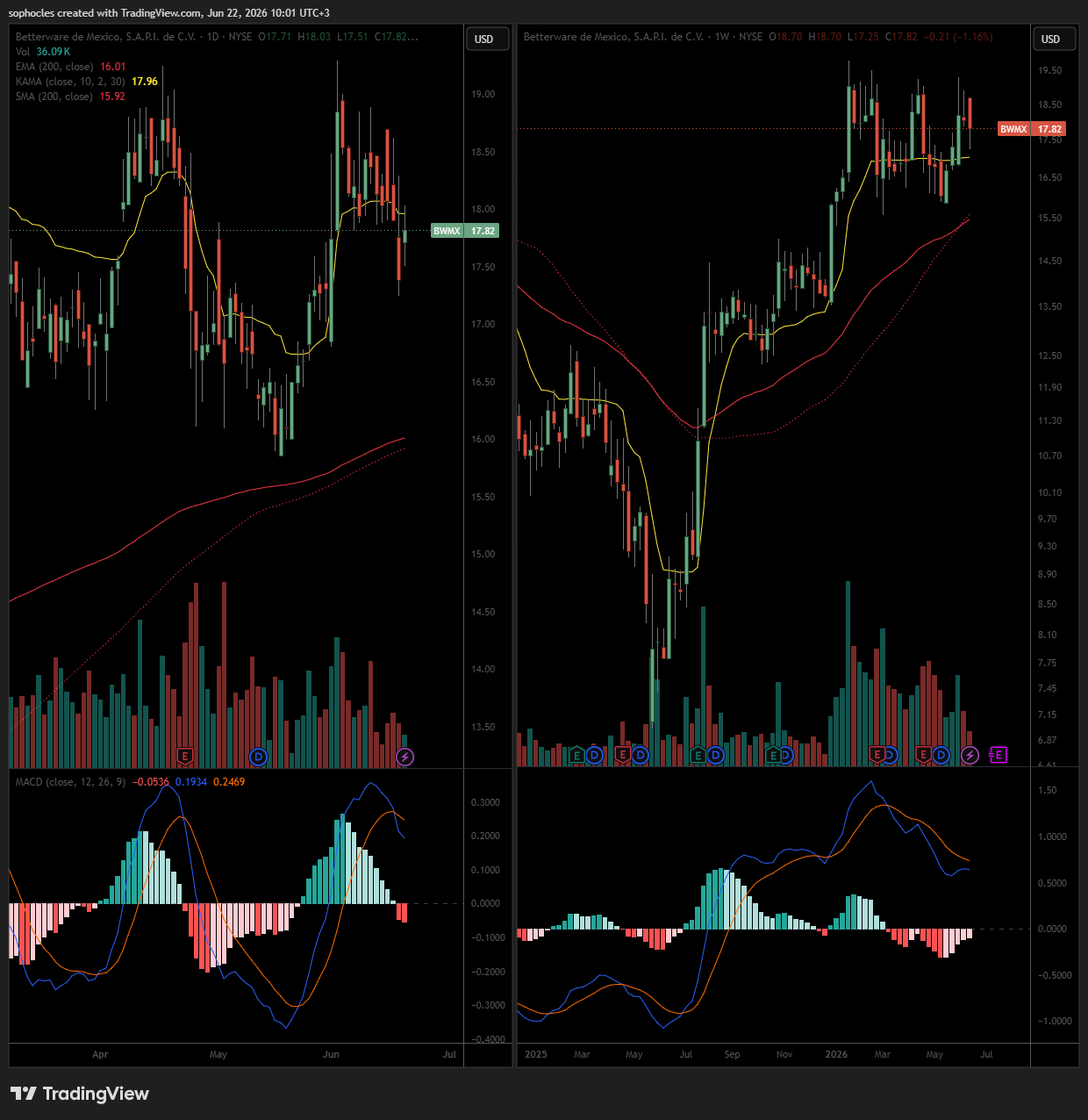

Betterware de Mexico, the DTC home goods company, did 130%. Despite the stock rise, the company still has a dividend yield of over 6%!

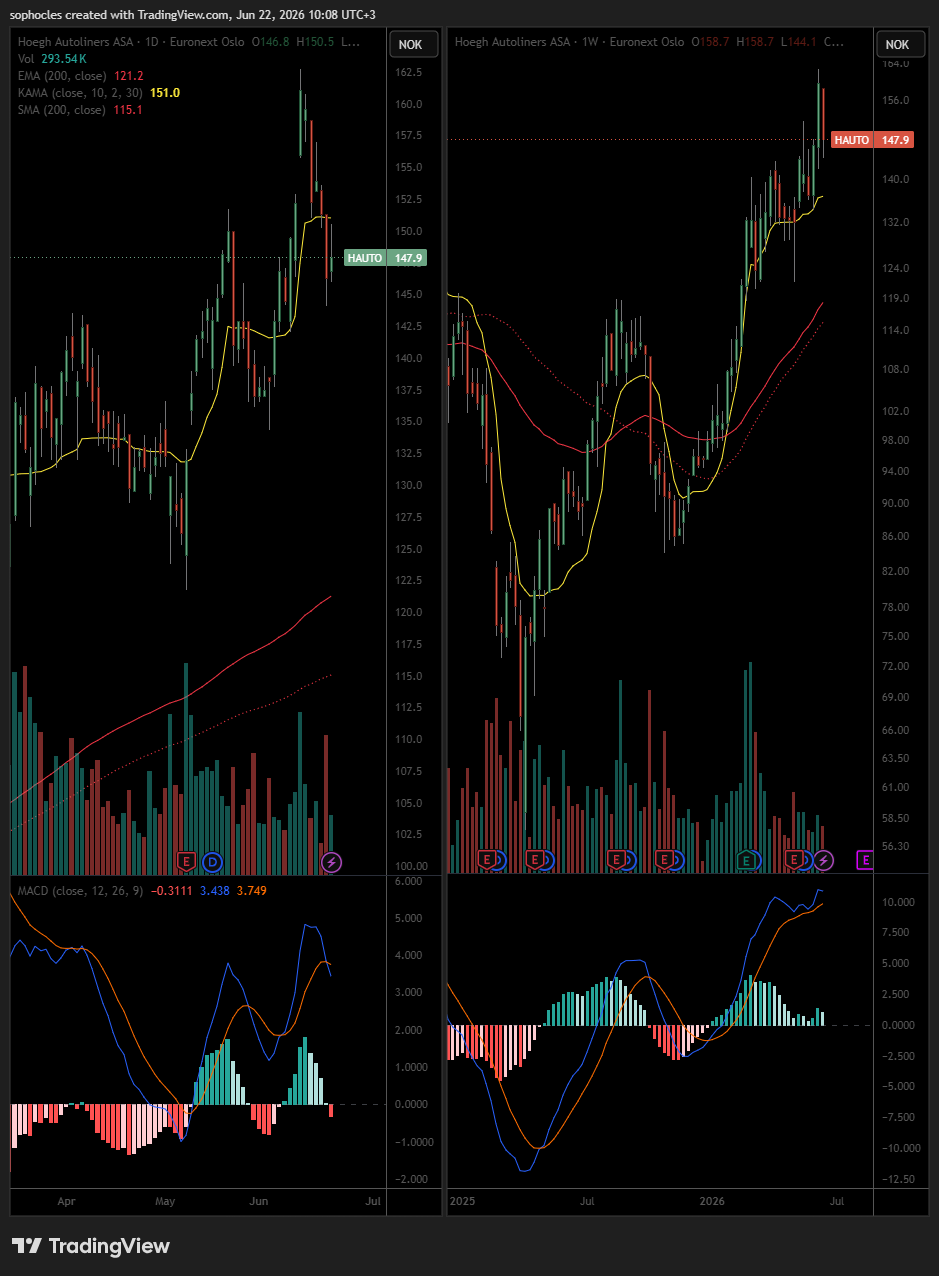

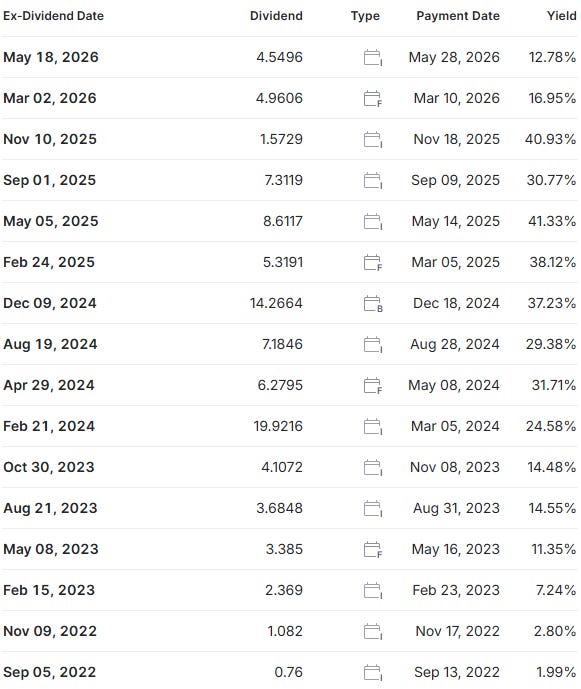

Ocean transport Höegh Autoliners did a total return of 111% in USD and 102% locally. It also has a massive dividend of 12%!

Probably worth checking out how sustainable it is. I definitely wouldn’t mind getting a double-digit dividend! Below is the dividend history per investing.com (link).

Below is the full list. Performance is shown in both USD and in local currency.

One reason I run screens like this is that they force me to look outside the usual list of popular stocks. That’s also why I focus all my events and podcasts on ideas. If you’d like to join me while I listen to 12 professionals pitch their highest-conviction ideas, check out the 3rd FatAlpha Value Online conference I’m hosting on October 22-23. Early bird ends June 30. The early bird includes:

• 12 LIVE pitches with audience Q&A

• 4 networking sessions

• Replay access to all presentations

• Private WhatsApp discussion group and forum access

• Early bird bonus: 6 recordings from prior events

Testimonials:

“Top-notch analysis and recommended companies. Deserves 10x the participants”

“Nice format: strong value; ideas seem uncorrelated to consensus”

Check it out: https://fatalphavalue.com/online

The Model

If you haven’t read the original article (here), my twists to Greenblatt’s popular screen are:

1. Instead of return on capital, I use return on equity for two reasons: a) ROC and ROIC can be defined differently by various screens and websites, while ROE is consistent, b) ROE stats are more readily available to investors.

2. I screen for companies that have a 20%+ ROE in each of the last 3 years. The purpose of that is to filter out companies with a temporary boost in ROE. Of course, this still doesn’t mean that these companies are great.

I started with c. 90 thousand equities listed in Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Greece, Hong Kong, Indonesia, Ireland, Israel, Italy, Japan, Luxembourg, Netherlands, Norway, Poland, Portugal, Singapore, Spain, Sweden, Switzerland, United Kingdom, and the United States.

After applying the 20% ROE threshold for the last 3 years, a market cap greater than EUR 100m, keeping only primary listings, and requiring a forward EV/EBIT multiple, I was down to 693.

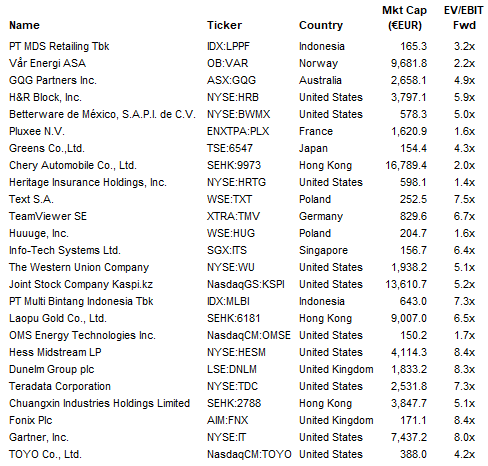

Each company got a score for EV/EBIT and a score for ROE. Each score places them in a bucket from 1 to 100, and then the scores were combined. The top companies are shown below.

Note that the following companies appeared both on this year’s list and last year’s: Betterware, GQG, H&R Block, Pluxee, Text, Western Union, Hess Midstream, Kaspi, PT MDS Retailing, and PT Multi Bintang Indonesia.

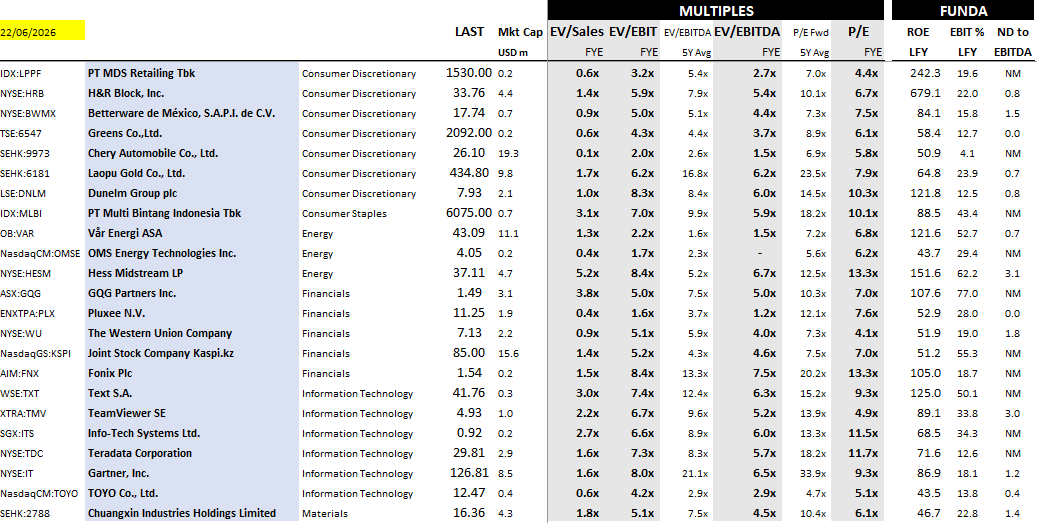

Multiples Table

Here is a summary table of tickers and forward multiples, sorted by sector. The market cap is in USD, while the ROE, EBIT margin, and Net Debt to EBITDA are historical. For perspective, the average EV/EBITDA and P/E multiples are also shown.

The Companies

Brief notes and stock charts on the stocks screened:

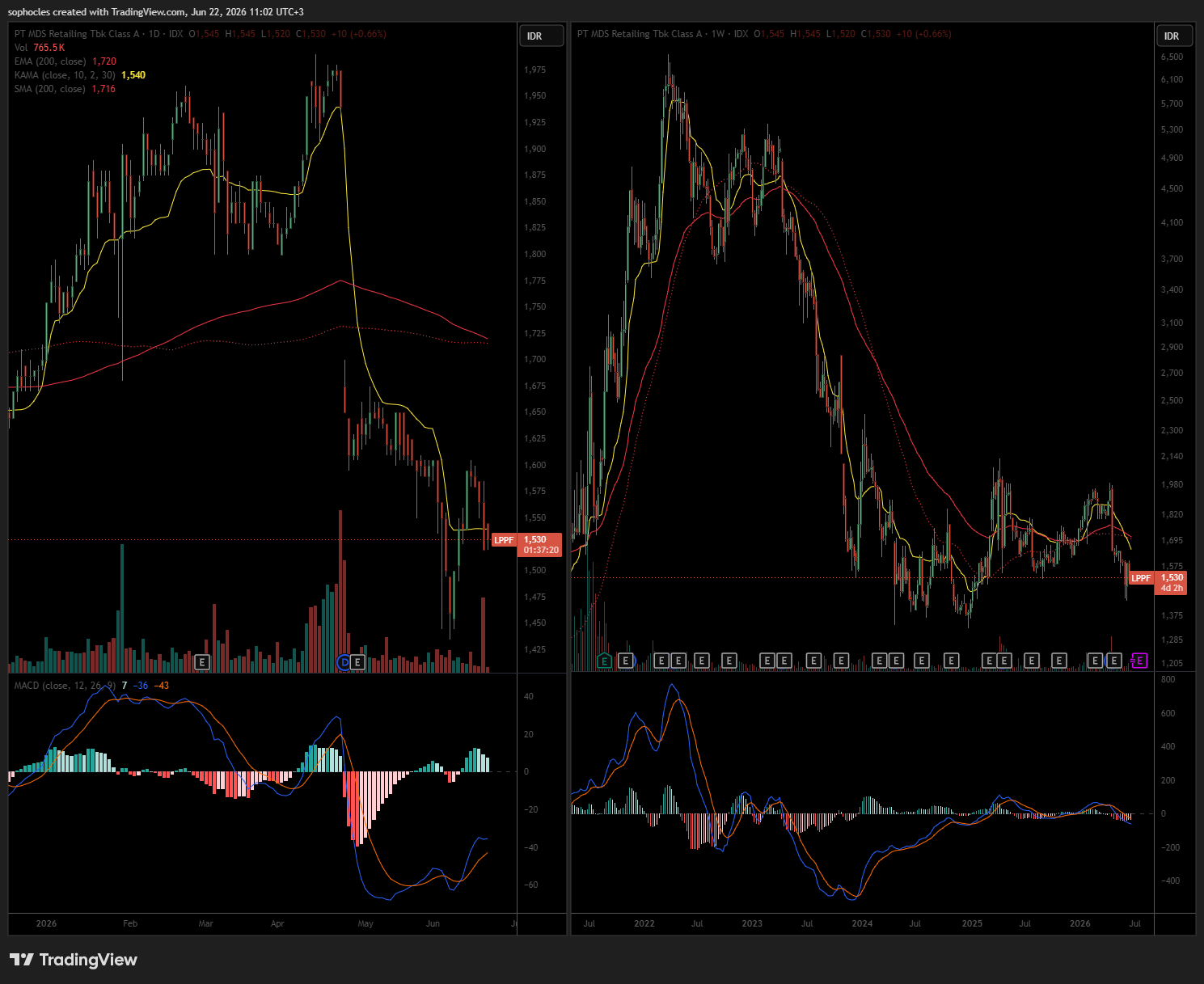

PT MDS (aka Matahari) is Indonesia's largest department store with c.150 stores in c.81 cities. The company has in-house private labels (Nevada, COLE, Connexion, Little M) and consignment/concession income, where third-party brands occupy the floor, and Matahari takes a cut. Retail is a tough space, so your entry price matters a lot imho. The recent gap-down was due to a large dividend (daily on the left, weekly on the right).

Var Energi is a pure-play upstream producer on the Norwegian Continental Shelf (NCS). It is second only to Equinor among NCS independents and majority-owned by Eni (c.63%). It’s a price-taker like most energy companies. Norway taxes upstream profits at a 78% rate but allows near-immediate expensing of capex and a cash refund of exploration costs. It pays a 11% dividend. You can check out the dividend history here.

GQG Partners is a boutique active equity manager (Global, International, Emerging Markets, US strategies) earning management fees on c.$160B AUM. Rajiv Jain is the CIO and owns c.70% of the company, so we have key man risk. The stock currently has a 14% dividend!

H&R Block is the largest assisted/DIY US tax-prep brand with c.$3.8B revenue that is highly seasonal (Q3, Jan–Apr), and split between company-owned and franchised offices. Earnings reported for the period ending March ‘26 surprised on both top line and bottom line. Stock popped but is currently retracing (see left chart). Dividend yield of 4.9%. Company competes with Intuit (Turbo Tax, Quickbooks), doing it yourself for free, and AI…

Betterware is a leading direct-to-consumer company in Mexico focused on home organization and beauty (Jafra). In April 2024, they launched in the U.S. to target the Hispanic population. The company has had 25 consecutive quarters of paying dividends since IPO, and says that they “maintain a 33% TTM Dividend-to-EBITDA ratio”. Leverage as been coming down with FCF is rising (1Q presentation). On an annual basis, revenue and EBITDA are flat.

Pluxee is the world's #2 employee-benefits platform (after Edenred), spun out of Sodexo in Feb 2024. Corporates fund prepaid benefit balances (meal/food vouchers, mobility, wellbeing) for c.37M employees that spend at c.1.7M merchants. Pluxee earns client fees, merchant commissions, and float income (interest on cash that sits c.7 weeks before it's spent). It's more of a pure-play (86% employee benefits) and more EM-weighted than diversified Edenred. Consensus FCF is EUR 352m vs a market cap of only EUR 1,600m. Brazil regulation and reform is the risk here, with S&P cutting its own forecast and management expecting lower revenues from the country.

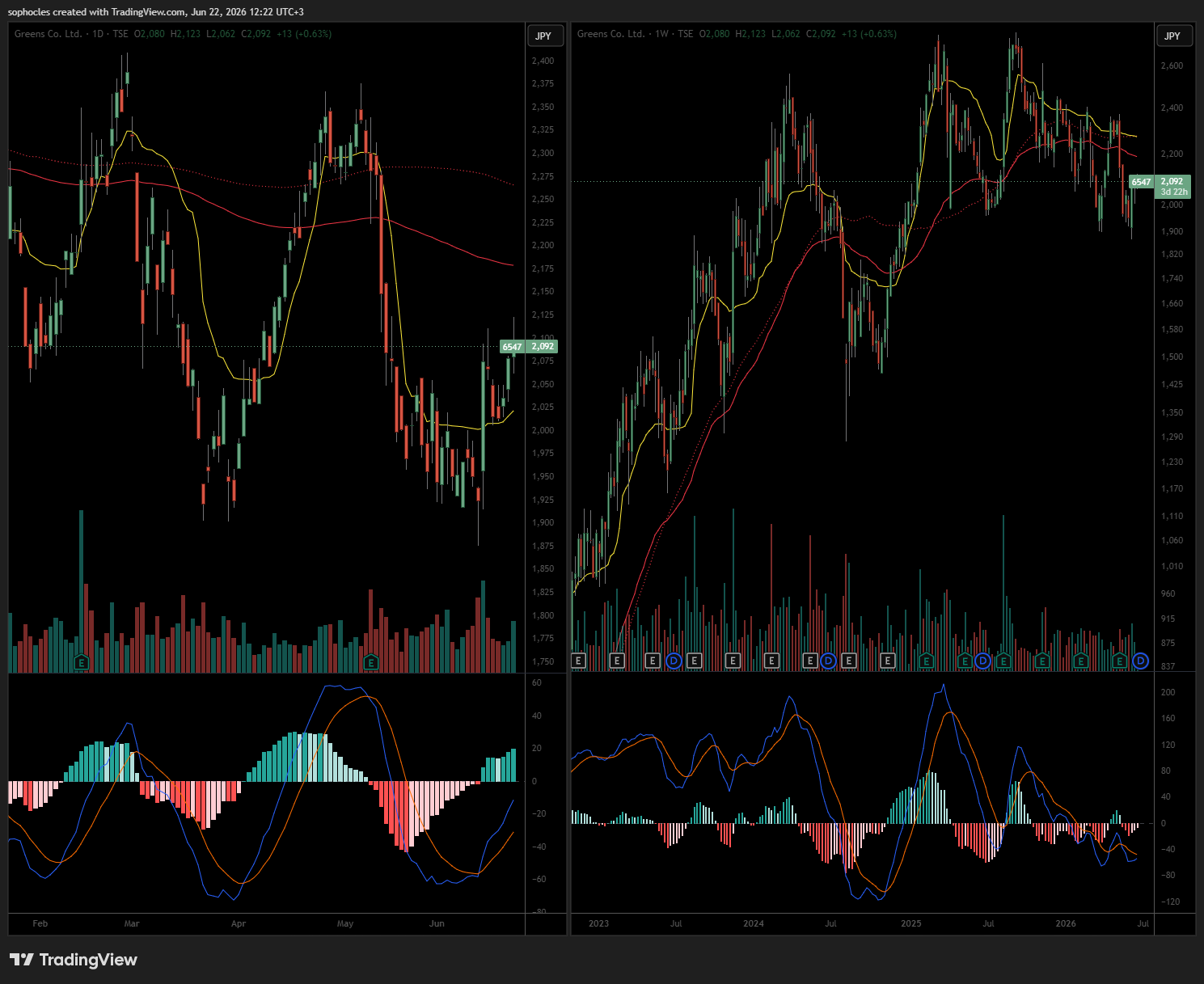

Greens is a Japanese hotel operator with an exclusive license from Choice Hotels International for the Comfort brand. This includes Comfort Hotel/Inn/Suites, leisure sub-brand Comfort Hotel ERA and the Ascend Collection. c. 100 hotels nationwide. Revenue grew 21% last year and is expected to grow 9% this year.

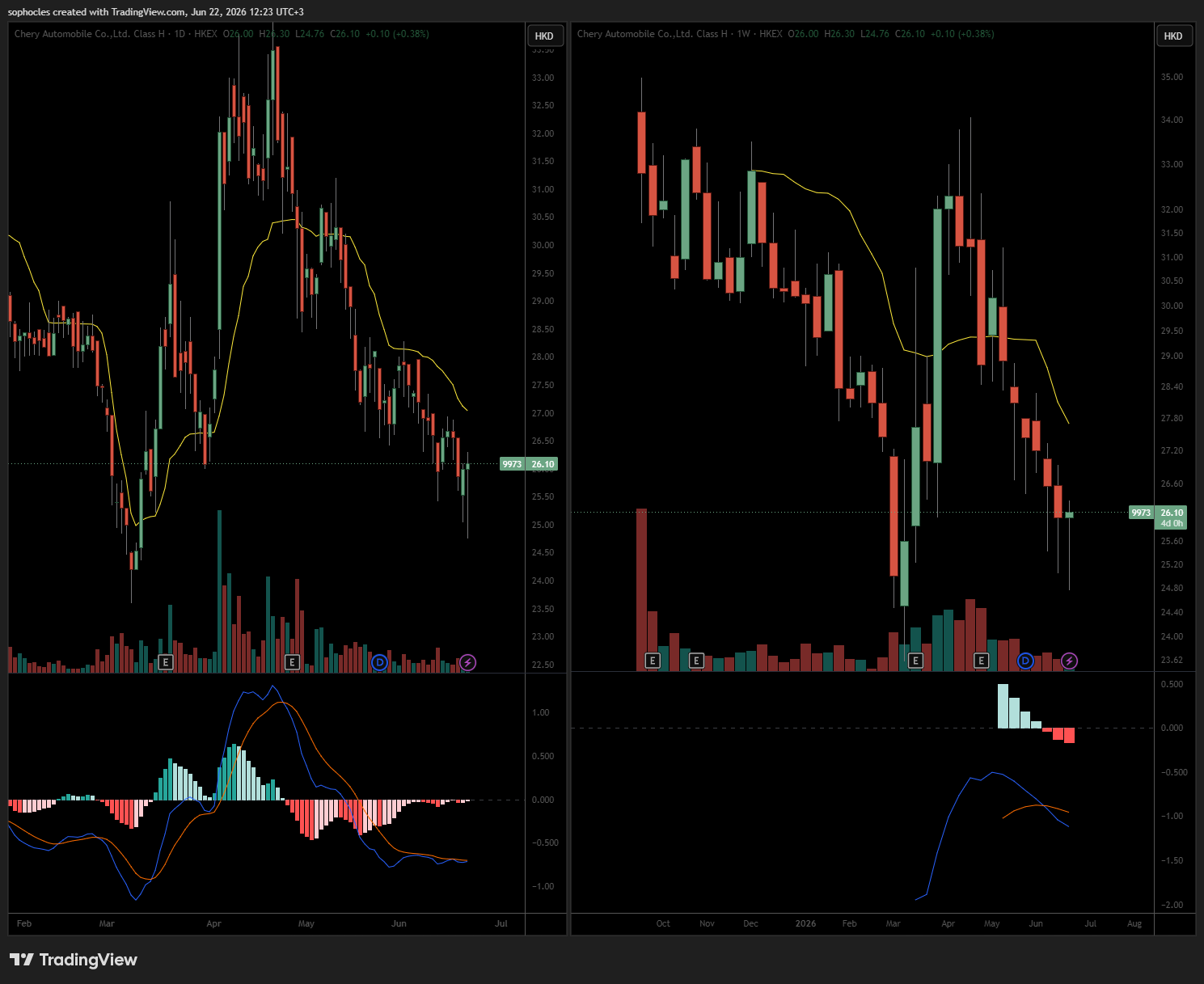

Chery Automobile is China’s #3 automaker by volume (c.2.8m vehicles in 2025). It sells ICE, hybrid, BEV, PHEV, and pure-EV cars across multiple brands. This includes Chery, Exeed (premium), Jetour (lifestyle SUV), iCar/iCaur, plus export brands Omoda/Jaecoo/Lepas. Over half of its revenue comes from exports, and it ships to 100+ countries.

Some time ago, I was looking at BYD, but I didn’t buy it because I saw how much competition there was in China. Reviews I saw put Chery vehicles as equivalent to BYD vehicles.

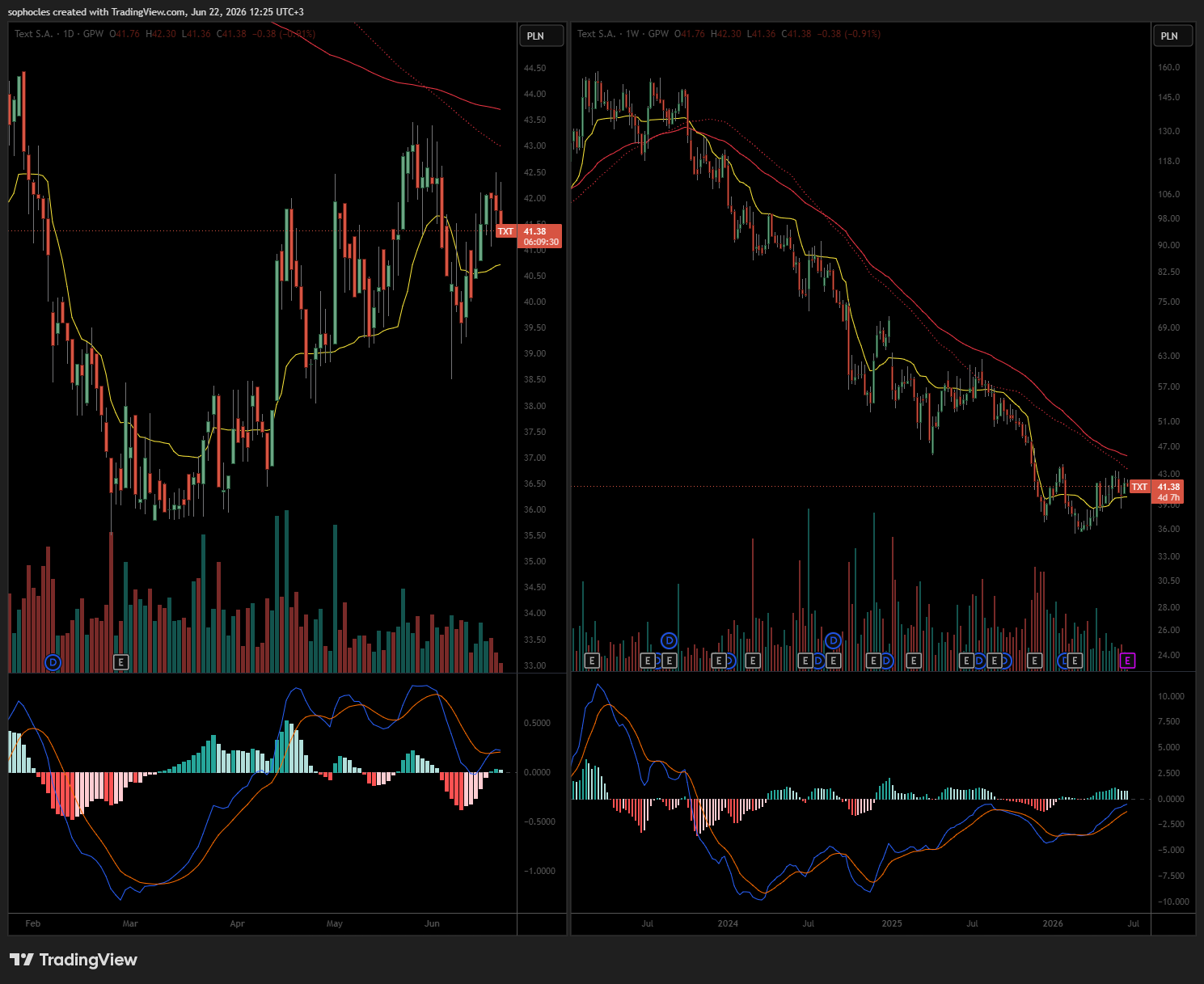

Text SA was a value trap I managed to avoid. It’s the Polish SaaS company behind LiveChat (flagship), ChatBot, HelpDesk, KnowledgeBase, OpenWidget, etc. It’s a commodity product that faced a lot of competition even before the explosion in AI. Revenue and margins dropped in the last quarter. Stock chart reflects this. Dividend at 13%.

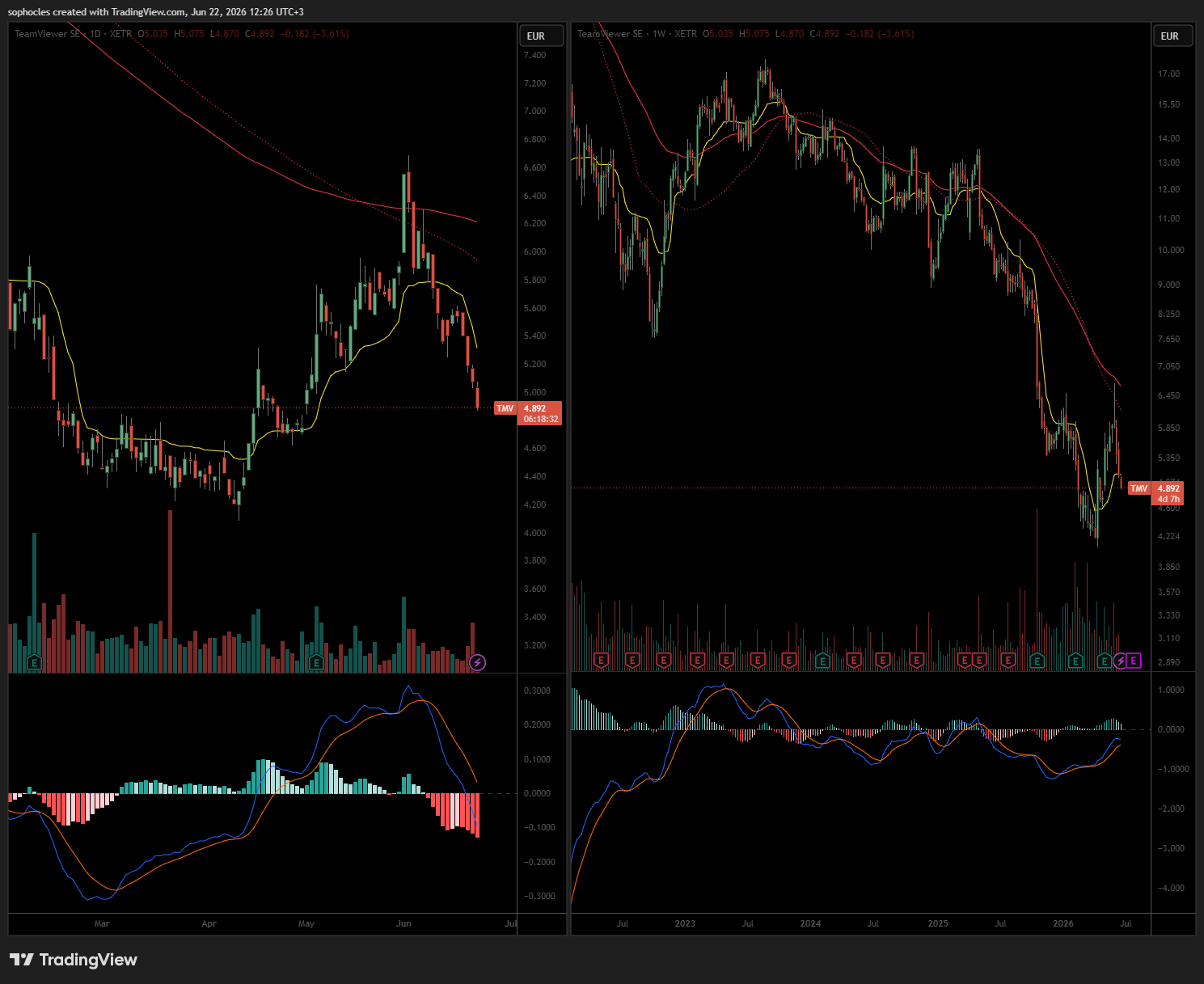

TeamViewer offers the well-known German remote-connectivity software. This is another stock that appears to have fallen due to AI. The argument being that less tech support will be needed due to AI assistance. PE firm Permira completely exited from the stock in September 2025 at EUR 9.20. At the time it was at a discount but it turned out to be a smart move. In 2026, the company was also a victim of a cybersecurity breach.

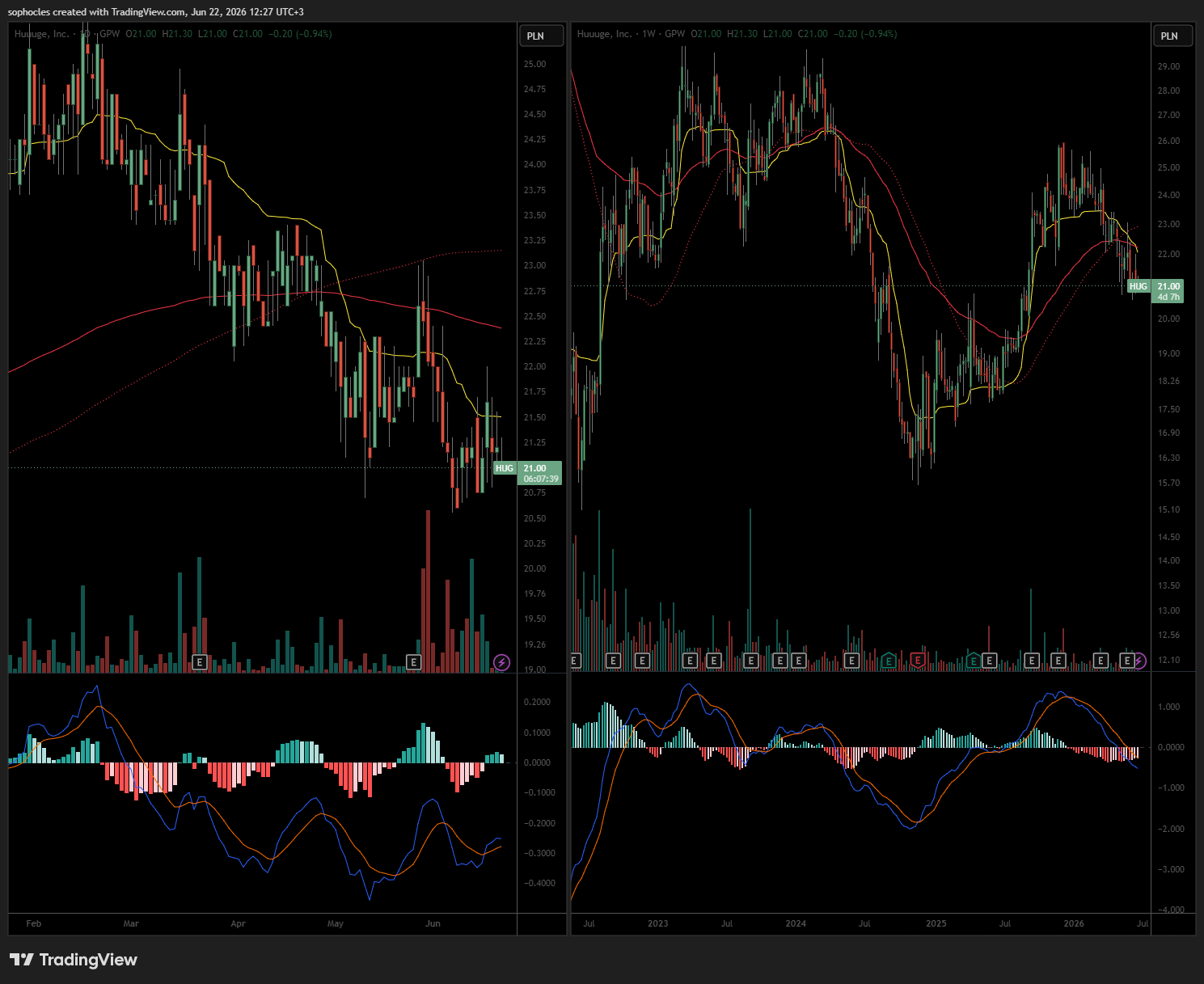

Huuuge, another Polish company, offers free-to-play social casino mobile games such as Huuuge Casino, Billionaire Casino (slots), plus Traffic Puzzle (casual). The company monetizes via in-app purchases and ads. Very competitive space with revenue and profits down in the last quarter. Regulatory risk as well.

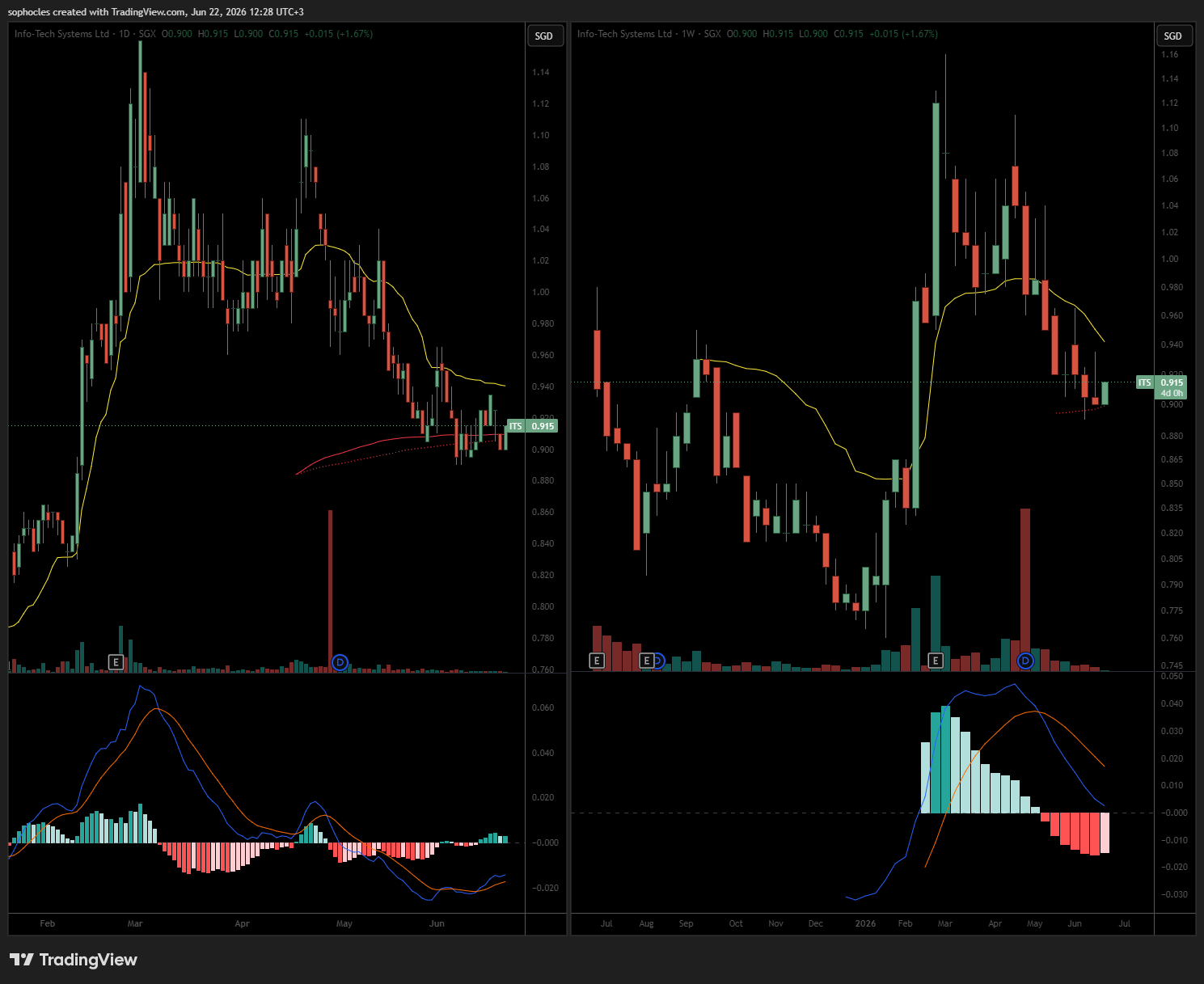

Info Tech Systems, headquartered in Singapore, offers HR, Accounting, and CRM software. Subscription-based, like most SaaS stocks, has taken a hit but analysts expect revenue growth to continue and margins to expand. Two insiders hold 61% (founders Dilip Babu and Peter Lee). The company IPO’d in July 2025.

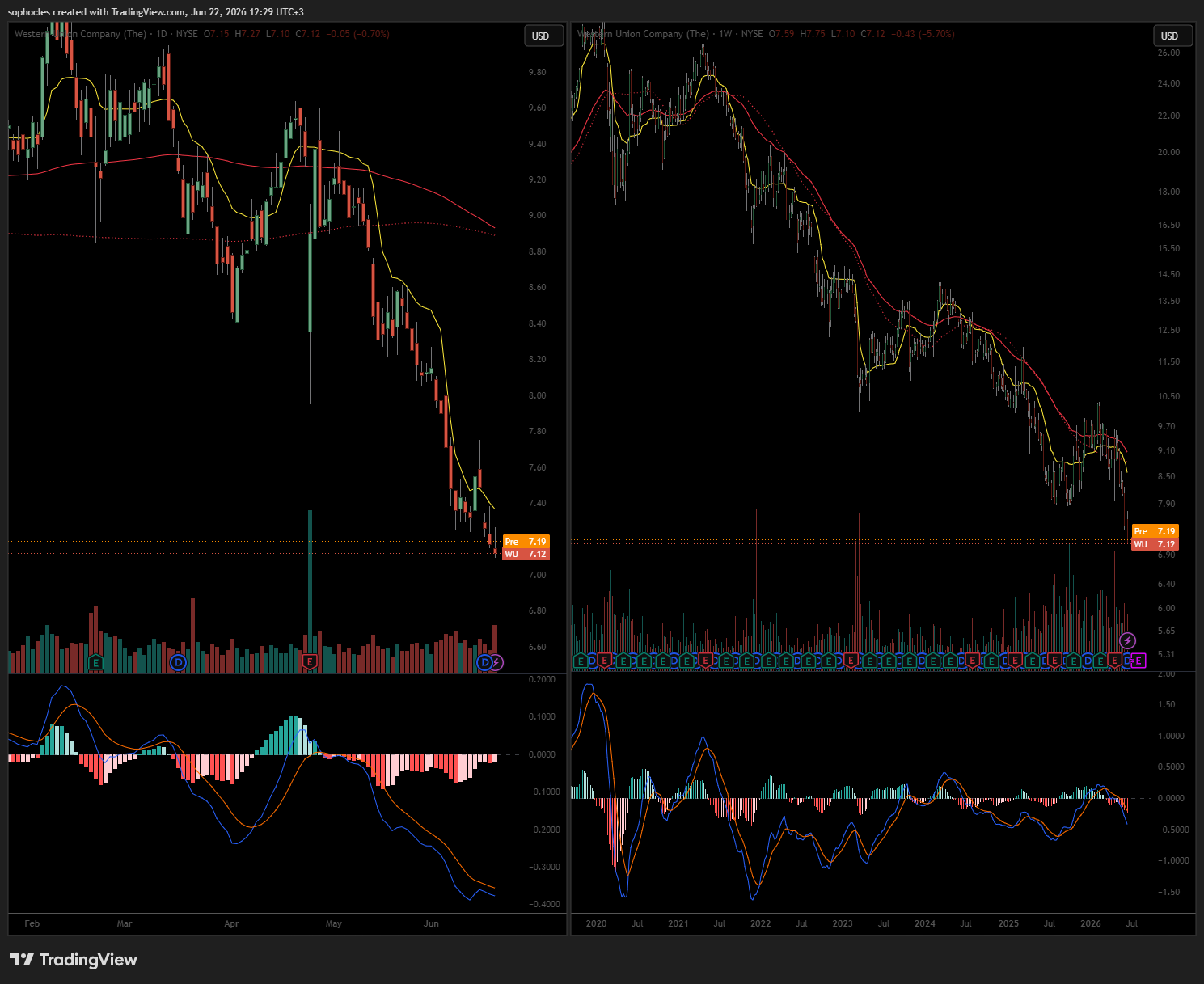

Western Union stock has been very weak, as the chart below shows. There has been no revenue growth, and margins have weakened over the past decade. Still generates, though, $500m+ FCF on $6.7b EV.

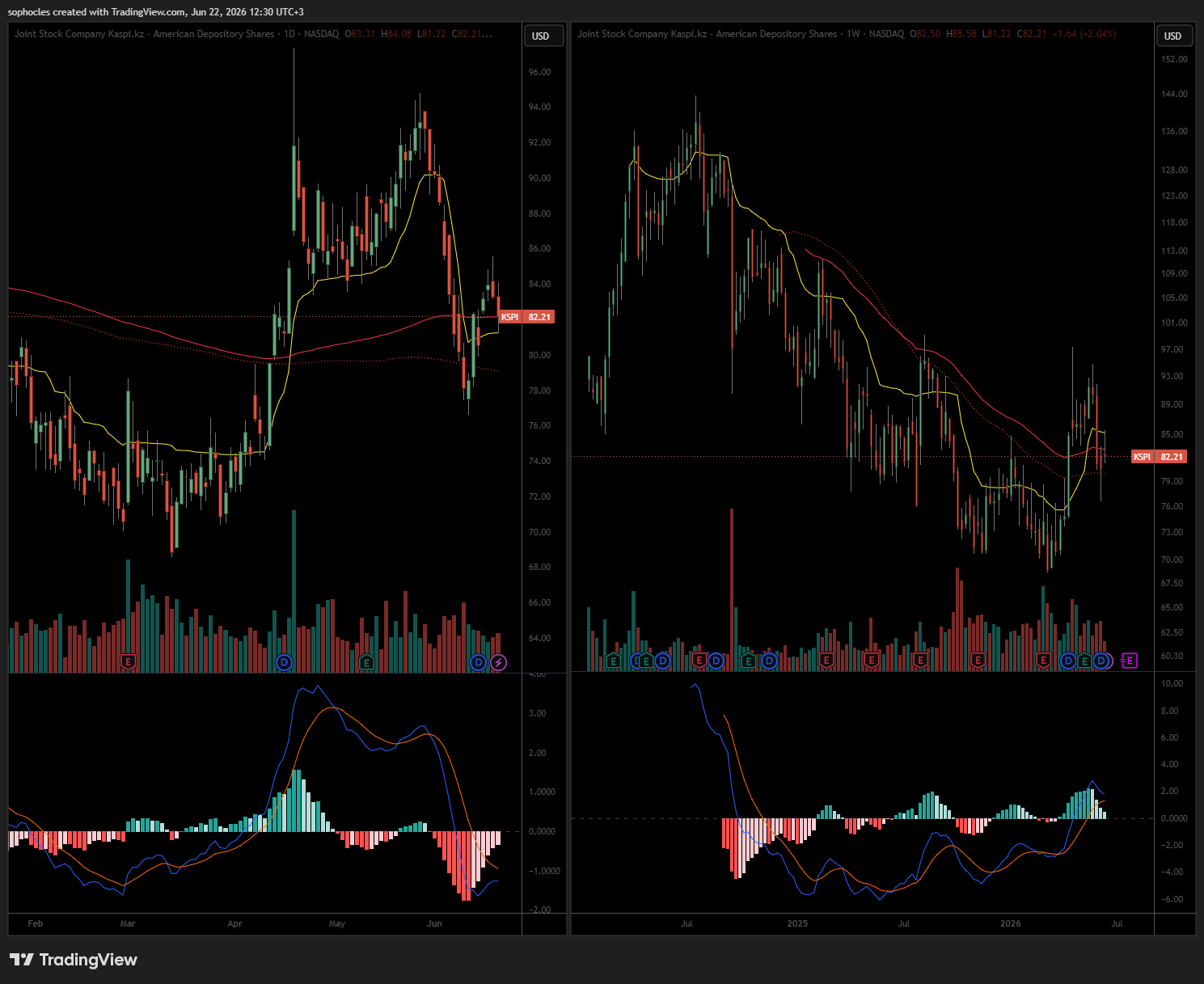

Kaspi used to be a darling among value investors. I too held it but took my profits after the Turkish acquisition, which I didn’t like. The fintech’s Super-App is the market leader in Kazakhstan, but as a bank, it sits in No. 2 position behind Halyk, which offers better value, imho.

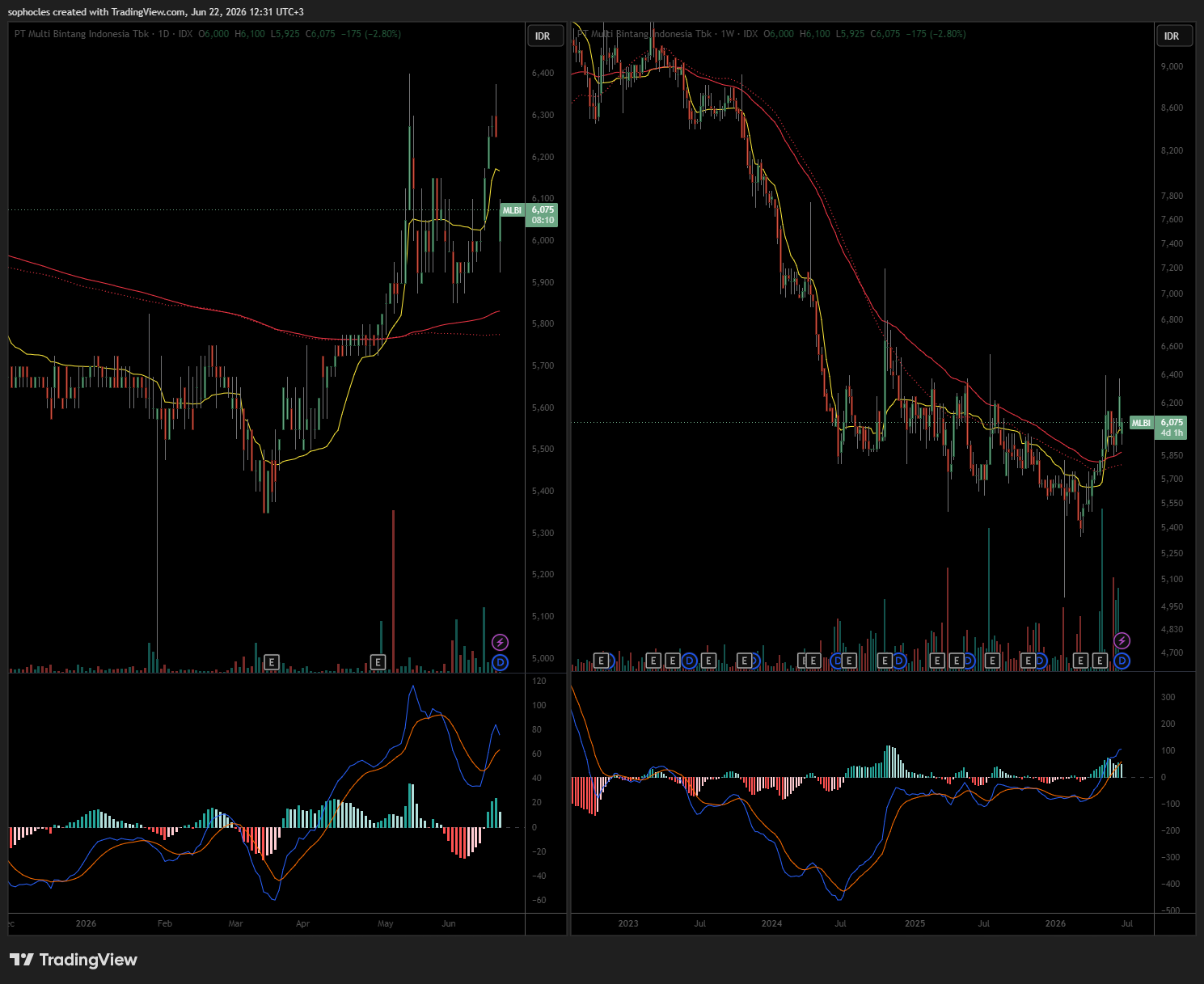

PT Multi Bintang Indonesia is the Heineken-controlled (83%) brewer that dominates Indonesia's beer market. Brands include Bintang (the iconic local lager), Heineken, Radler, Strongbow cider, and Bintang 0.0. The 9% dividend yield makes this interesting, but you have to keep in mind your IDR exposure. The IDR has already lost 6.3% in value in 2026, while the company is projected to drop top line by 7% for the entire FY26. Entry price makes a huge difference on this one.

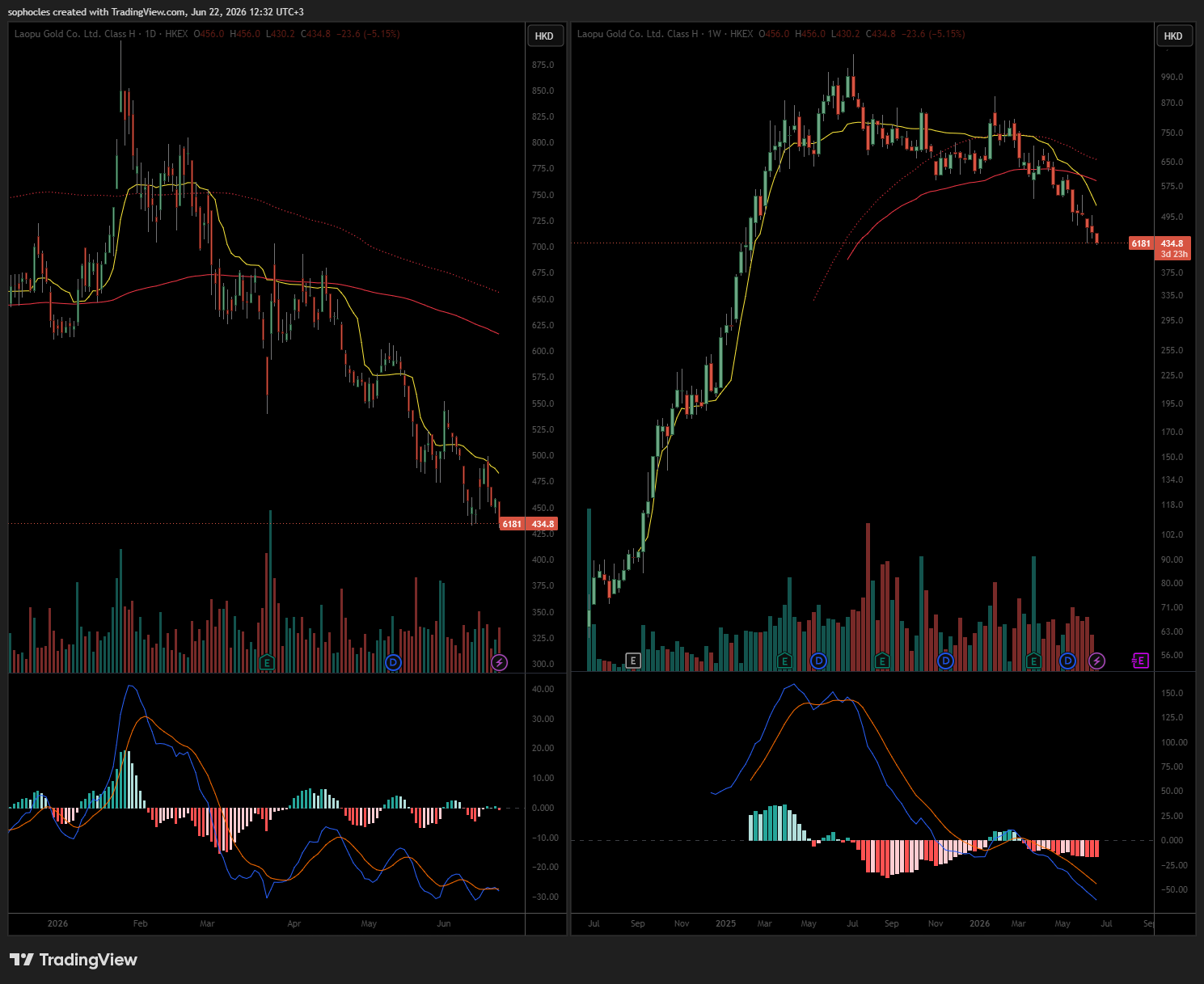

Laopu Gold has positioned itself as the Tiffany/Hermes of gold. It focuses on Chinese “heritage-gold” using "ancient technique" to hand forge luxury jewelry sold at a steep premium to weight. Top line has grown in the triple digits in each of the last 3 years, while analysts expect FY26 to grow at 55%! The stock trades at 9x forward earnings.

OMS Energy Technologies is a Singapore-based oilfield services and manufacturing company (click here to see products). They did a Nasdaq IPO in May 2025.

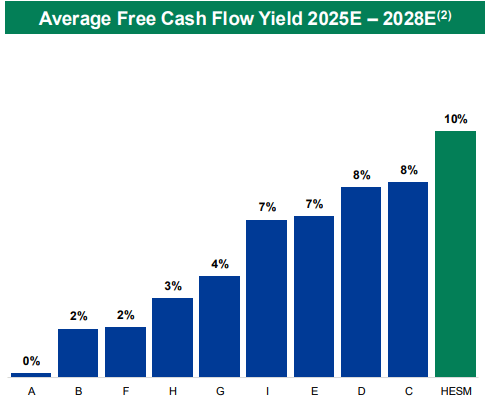

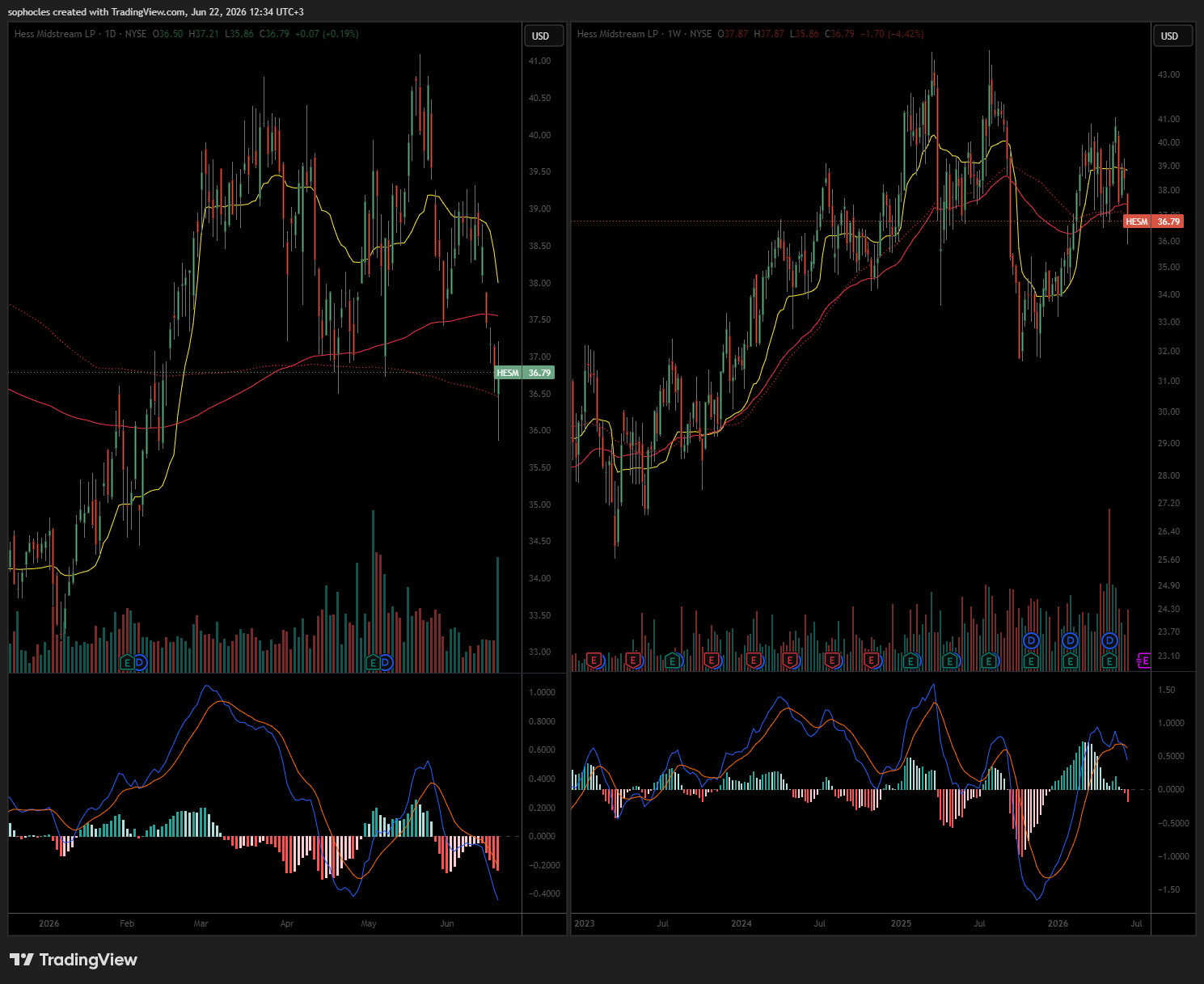

Hess Midstream is a midstream operating focused on the Bakken (North Dakota) region. Post July ‘25, its main customer, and 37.7% owner, is now Chevron (which acquired Hess). Per their IR presentation (here), they have the highest FCF yield among peers.

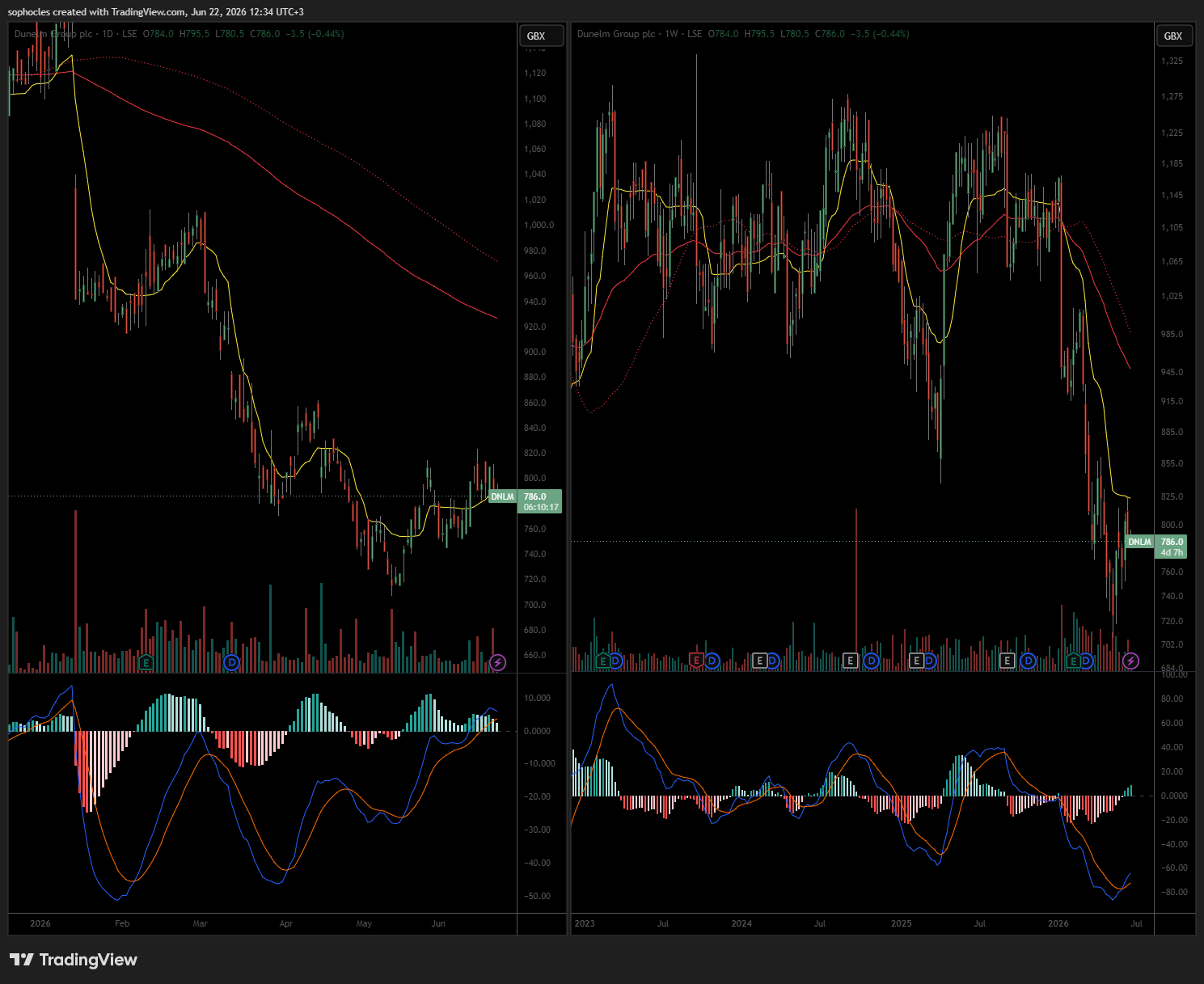

Dunelm Group is a UK home furnishings retailer with c. 200 stores. They sell mostly own-brand products. It’s family-controlled (Adderley). EPS has been flat for the last few years.

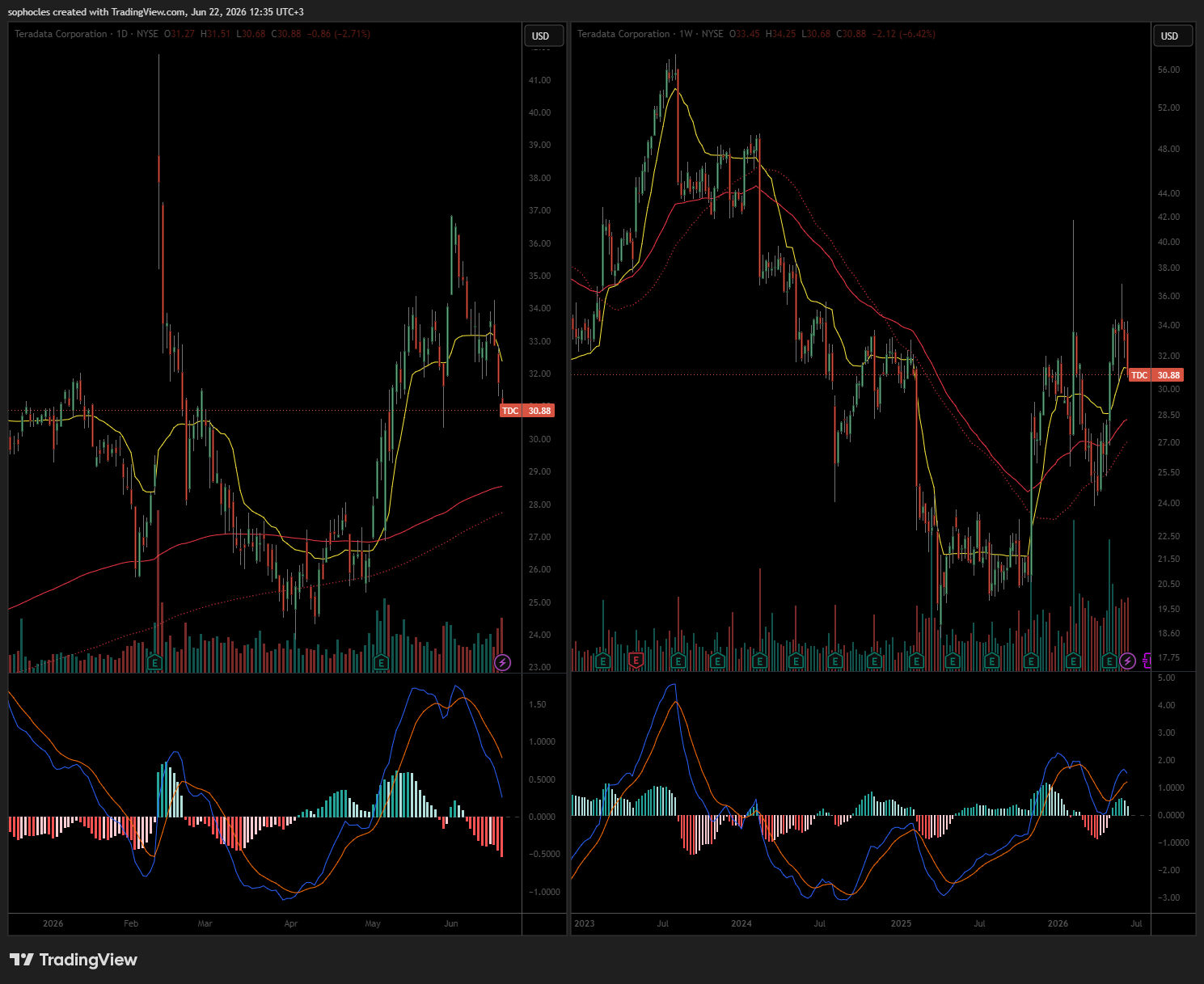

Teradata Corp is an enterprise software company that develops and sells database analytics software. Going forward, revenue is expected to be flat.

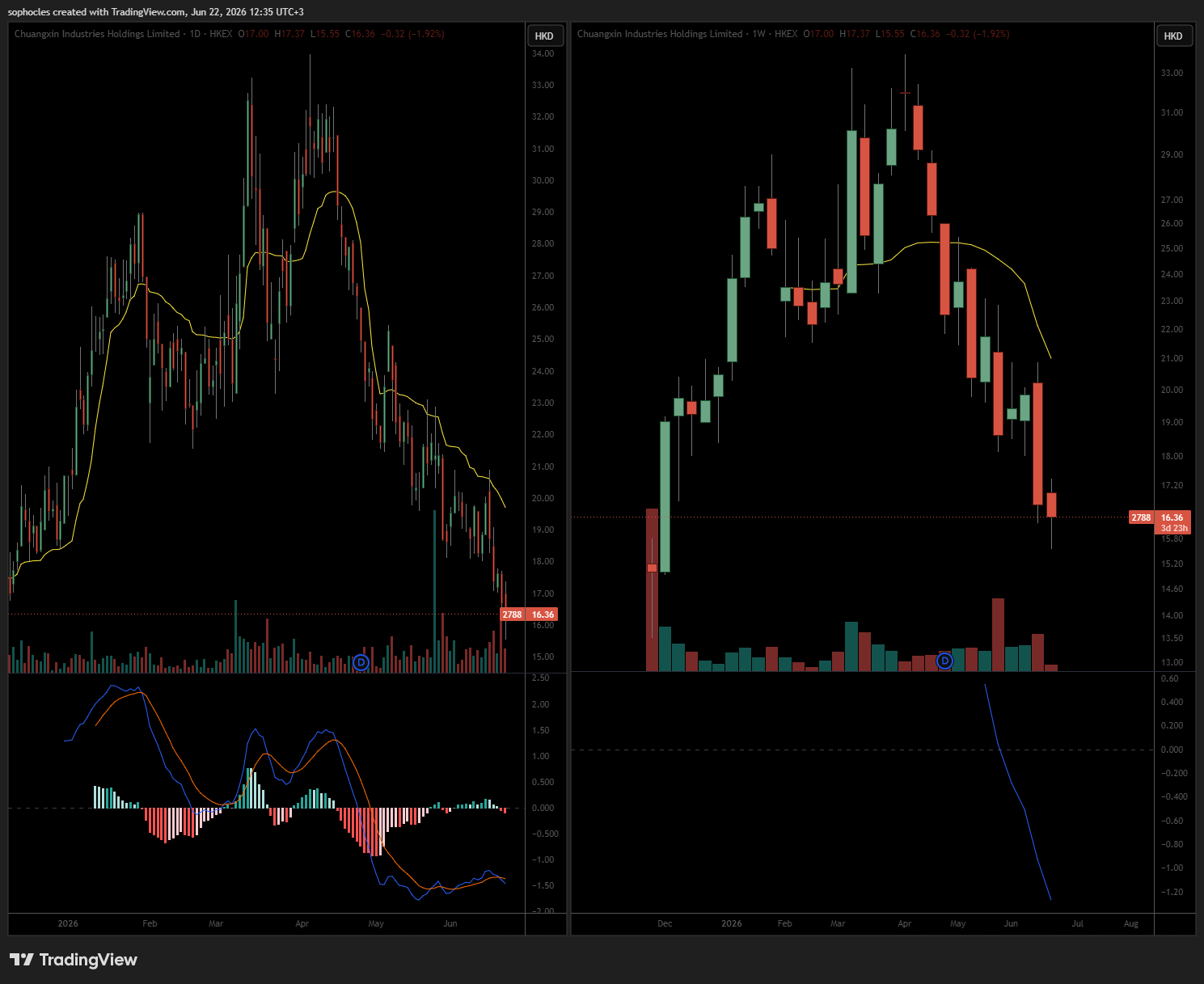

Chuangxin Industries Holdings is a Chinese vertically integrated aluminum producer that is powered by wind and solar.

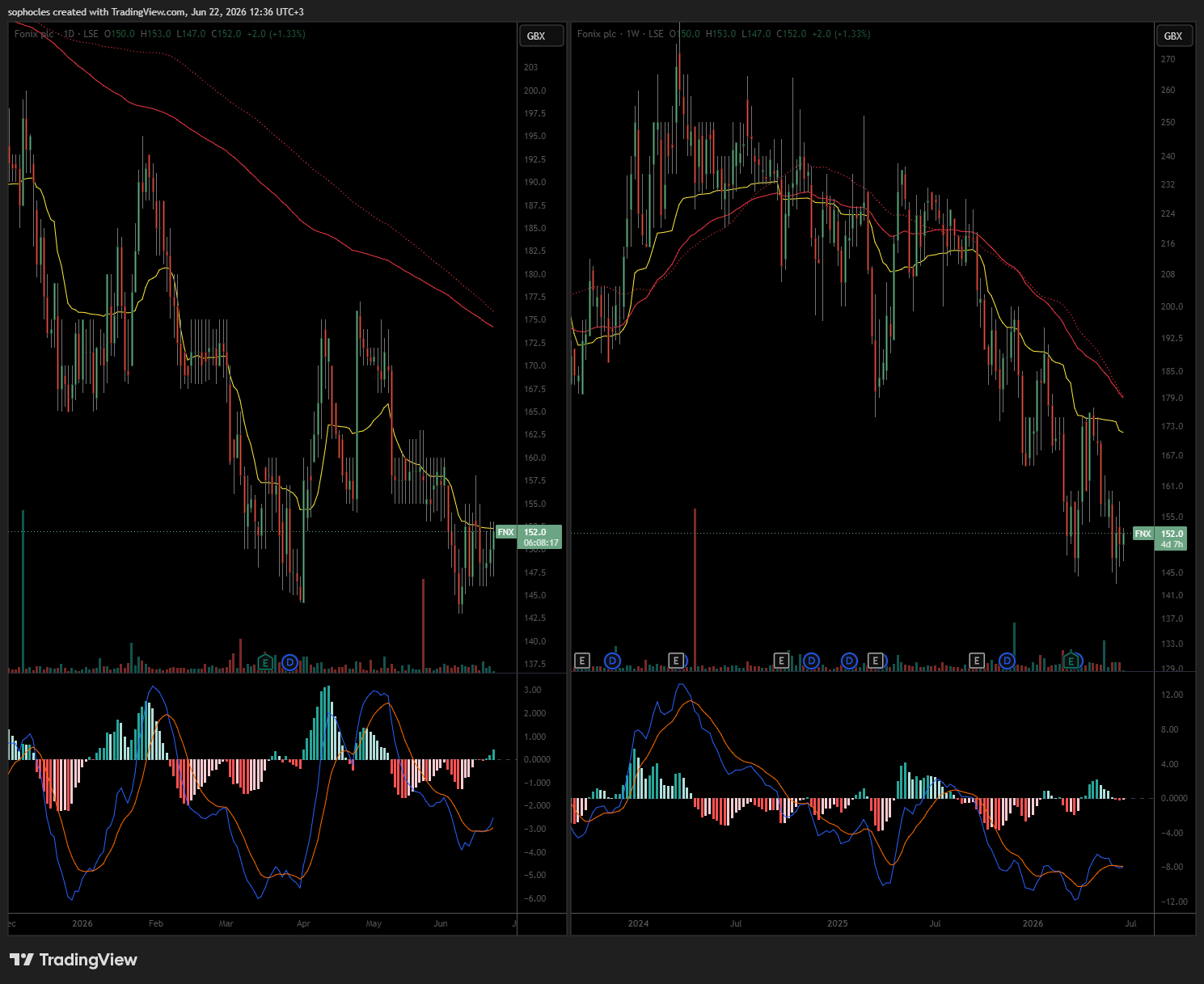

Fonix’s main revenue driver (c.64%) is its mobile payments. Its platform allows consumers to purchase digital content, enter competitions, deposit cash, or donate to charity by charging the transaction directly to their mobile phone bill or deducting it from pay-as-you-go credit. Top line was growing at double digits annually until 2024. 2025 saw a decline in transaction volume, which resulted in a -4% decline in revenue. Going forward, growth is expected to return. Looks like an interesting little niche business which screens like this can pop up.

Gartner, the famous research and consulting firm, made the list. The stock saw a strong post-COVID rise, from under $100 to over $500. The brand is well known, and the stock is currently trading at an FCF/EV yield of c. 11%. The risk is that budgets will be redistributed due to AI and reduced consulting spend going forward.

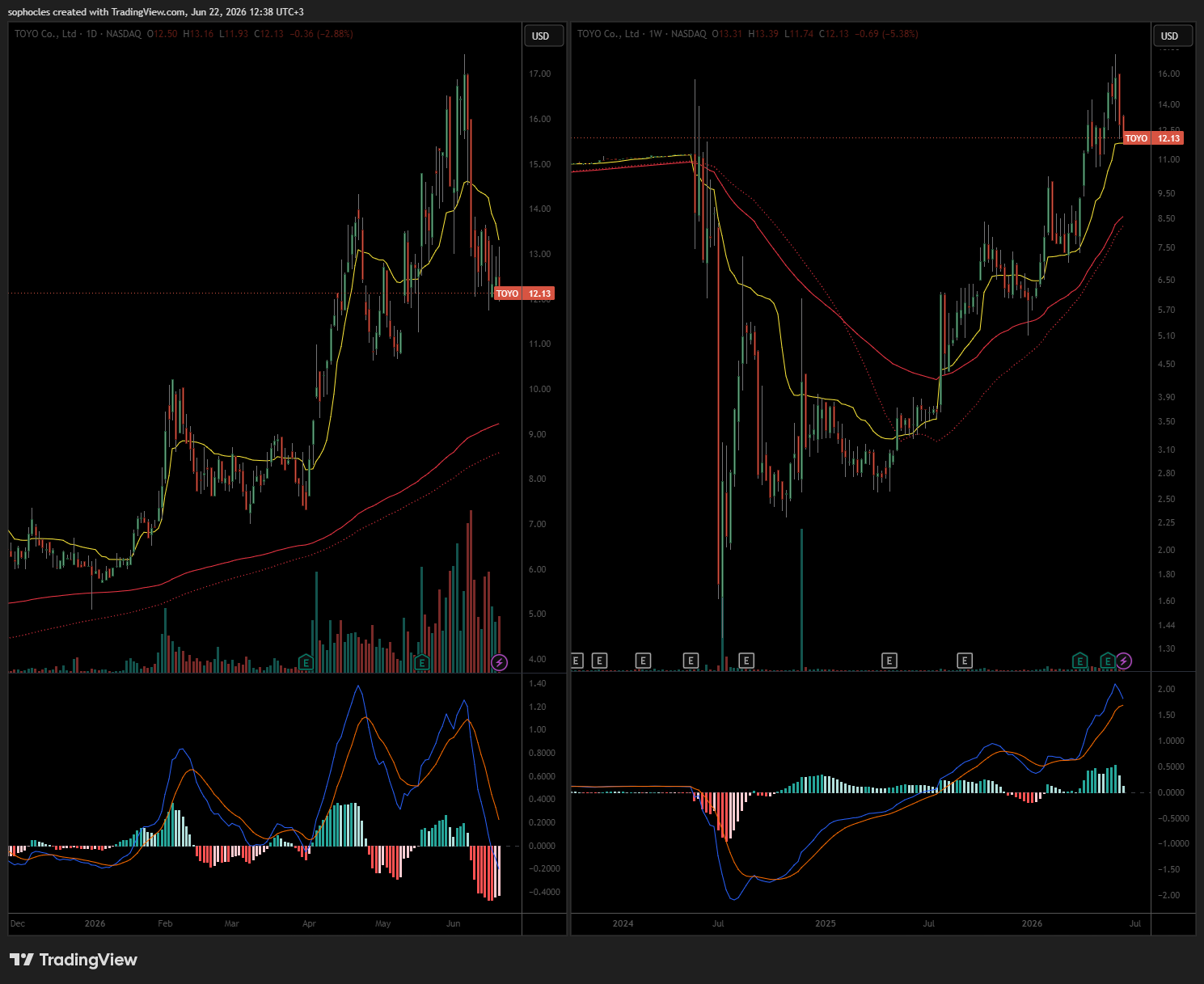

TOYO is a Japanese-headquartered solar manufacturer that listed through a SPAC. They are building a 1.5 GW solar cell facility in Houston that will enable them to bypass tariffs on Chinese solar imports.

Any of the companies in this list look interesting to you?

Would you like me to share more screens?

Let me know in the comments!

Don’t forget to check out the Online event, as the early bird expires at the end of the month —> https://fatalphavalue.com/online

Good luck!

Sophocles

Disclaimer: Not investment advice. Do your own work! This account is not operated by a broker, a dealer, a registered investment adviser, or a regulated entity. Under no circumstances does any information posted represent a recommendation to buy or sell a security. In no event shall the author be liable to anyone reading this post for any damages of any kind arising out of the use of any content available in this post. Past performance is a poor indicator of future performance. All the information on this substack and any related materials is not intended to be, nor does it constitute investment advice or a recommendation. All materials and information you obtain here are exclusively for informational purposes and do not constitute an offer or solicitation to provide any investment services to investors based in the U.S. or elsewhere.